Inflation sinks as bulls don’t blink | Luminor

Inflation sinks as bulls don’t blink

- Inflation drops – worries remain

- Russian moves revive food inflation fears

- Chinese economy slows

- Technology companies’ earnings mixed

During July markets have been digesting the next leg in falling inflation figures and news on mixed macroeconomic picture in different markets. Developed markets’ stock index MSCI World (EUR) has risen by 3,29%, while emerging markets stocks’ index MSCI Emerging Markets (EUR) has added 5,8%. At the same time, bond yields have risen slightly, too, with 10‑year US Treasury yields rising to 3,95% (3,84% 1 month ago), while German 10‑year Bund yields ended at 2,49% (in comparison to 2,39% a month ago).

Inflation drops

United States has continued showing encouraging signs of easing inflation. Measured by Consumer Price Index (CPI), Year‑on‑Year (YoY) inflation has dropped to 3% on June reading – lower, than expected by the market participants (3.1%), sharply down from 4% a month ago and long way down from the record 9.10% reported last year. This marks the slowest price rises in the worlds’ largest economy since the 2021 Spring. In its July meeting, FED (Federal Reserve) decided to raise interest rates by another 0.25% to 5.25‑5.50% ‑ a move believed by some market participants to be the last hike for the foreseeable future. In a slight contrast to the US news, Eurozone inflation figures came in higher‑than‑expected at 5.5% (vs 5.4% expected) – itself sharply down from the 10.6% level seen last year. Also, ECB (European Central Bank) raised rates by 0.25% to 3.75% with the real probability of raising it again in September. With that in mind, currency markets have been rather volatile with EUR/USD currency pair showing sharp moves in the 1,09 – 1,12 range.

Food inflation worries revived

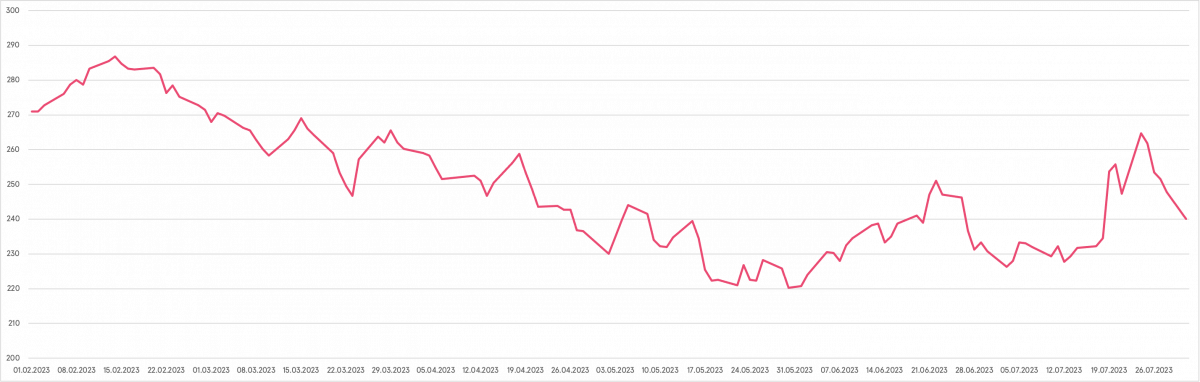

Policymakers have long been worried about the tight labor markets (hence, pressure for higher salaries), stubborn core inflation figures etc. in their inflation struggle. In turn, Russian decision to drop out of the UN‑backed Ukraine grain deal in July could only prolong the list of potential factors in the inflation story. Russia’s exit from the deal, then measures to limit the grain vessels’ movement in the Black sea and then finally targeting the grain infrastructure on the Ukrainian Black Sea ports could potentially curb the Ukrainian grain exports. As tensions escalated, wheat price popped by almost 18% in July (September deliveries, European market). Should these circumstances continue, this will sure add the pressure on the food‑related commodities prices to rise, thus undermining the otherwise mostly successful downward movement in global inflation, so far.

Milling Wheat (Sep 2023 delivery) price, EUR/t

Chinese economy slows

At the same time, Chinese economy – the bellwether of the Emerging Markets – has been showing further signs of economic slowdown. Thanks to lower level of economic activity last year (due to Covid 19 measures, at the time), the economy grew 6.3% YoY, sharply lower than 7.3% forecasted. That comes in unsurprising bearing in mind the 8.3% YoY drop in exports, sharply slower retail trade growth (3.1% YoY vs 12.7% YoY growth in May) and slow real estate market. Curiously, a record 11.58 million of fresh Chinese universities’ graduates are entering the workforce this year. They are apparently off to a rough start in their careers, as the youth unemployment in China has reached a record 21.3% (roughly double the 2018 level & double the current US level). While this high level of unemployed young people is actually comparable to the Southern Europe levels, this is a new phenomenon in China and will further signify the economic challenges that China is facing.

Not all tech doing great

This year’s rally in equities has so far relied heavily on technology‑related companies, thanks to much‑hyped investor expectations about Artificial Intelligence (AI). With earnings’ season in full swing, many companies have managed to keep up with the high bar of expectations, although not without the disappointments. Taiwan Semiconductor Manufacturing company limited (TSMC) – the largest chipmaker in the world by market value – lowered the outlook for 2023, as the AI‑related demand may not compensate the otherwise slower global demand for chips this year. Thanks to US‑China tensions, investors were not too excited about the earnings of another major name in the AI story, Dutch ASML, which is a leading player in the semiconductor industry, globally. Lastly, some market darlings, like Tesla or Netflix have slipped sharply (‑9.7% and ‑8.4%, respectively) after posting disappointing results. While that may not represent a market‑wide trend, episodes like that will get investors pickier about the technology companies’ prospects, going forward.

Market view

While there has been no major stance change, our investment team has been closely following the developments in the inflation trends coupled with economic prospects. A rather neutral market‑positioning is due thanks to the balanced‑out factors on the positive and negative in the foreseeable future.

Luminor House View

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.