Dancing on the edge of irrational exuberance? | Luminor

Dancing on the edge of irrational exuberance?

- Interest Rate expectations in focus

- Earnings slide back into the spotlight

- Shipping disruptions in the Red Sea

In a bustling month marked by central bank activities, economic updates, and earnings releases, investors are gearing up for a dynamic period. With the earnings season gaining momentum, a keen focus is on identifying which companies thrive in the current environment and which struggle to sustain both top‑line growth and margins. Notably, enthusiasm for artificial intelligence (AI) serves as a key driver. The surge in demand for high‑end chips essential for AI applications has heightened optimism. Simultaneously, the persistent narrative of a "soft landing" remains prevalent, allowing markets to reach all‑time highs while also moderating expectations for Federal Reserve (Fed) rate cuts.

As a result, developed markets’ stock index MSCI World has increased 2.91%, while emerging markets stocks’ index MSCI Emerging Markets has dropped by 3.03%. During the same period yields on bonds have increased slightly, with 10‑year US Treasury bond yields rising to 4% (compared to 3.87% 1 month ago) and German 10‑year bond yields increasing to 2.17%, up from 2.02% a month ago.

Central Banks at Crossroads

The European Central Bank (ECB) held interest rates at 4%, stating again that they are committed to fighting inflation, even though they are getting ready to make borrowing cheaper. In post‑decision press conference, ECB President Christine Lagarde highlighted a shared view among decision makers that it was too early to consider rate cuts. She emphasized that future decisions would be dependent on incoming data. The ECB might wait for data that consistently shows a slowdown, review things in March, and be sure before deciding on a rate cut in June.

The Federal Reserve concluded its January policy meeting by deciding to keep its policy rate unchanged, as most investors expected, so attention shifted towards the Fed's tone and its outlook on future policy actions. Even though FOMC (Federal Open Market Committee) members voted to keep the benchmark rate within the target range of 5.25%‑5.5% for the fourth consecutive meeting, Chair Powel introduced significant changes to its statement. Despite noting a decrease in inflation that could lead to interest rate cuts this year, the market reacted unfavorably to Fed Chair Powell's remarks, indicating skepticism about the likelihood of a rate cut in March. The statement turned out to be more hawkish than expected, with the Federal Reserve firmly resisting the market's more optimistic outlook. Therefore, the general expectation is for rate cuts to begin in May 2024, based on the current outlook.

Tech to remain a standout

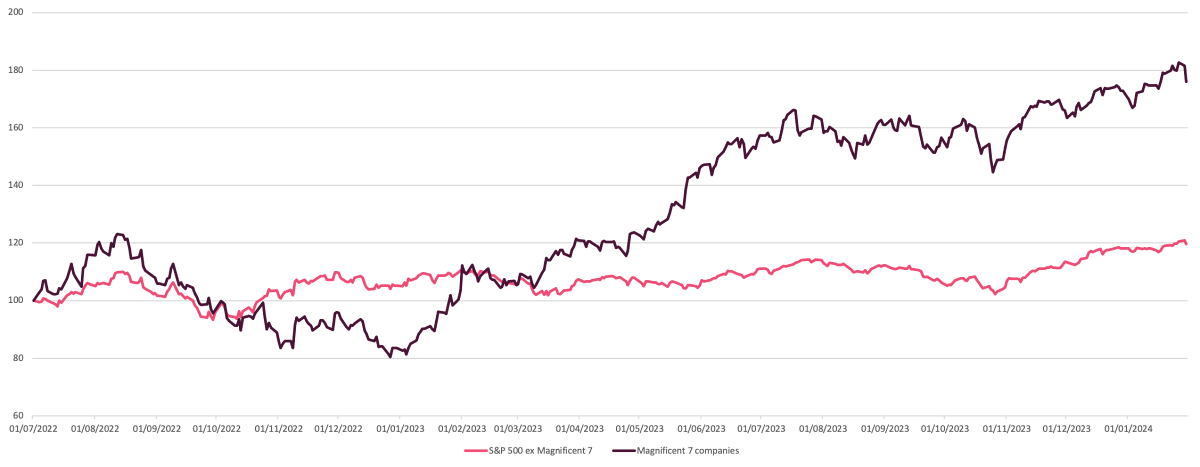

Technology had a major impact on the market last year, with big tech companies continuing to wield significant earning power. This led to tech‑related sectors performing significantly better than others. Despite concerns about these sectors’ stocks being expensive, their success appear to be grounded in solid fundamentals. In the fourth quarter, tech‑related sectors are expected to excel in terms of earnings. While the rest of the more “traditional” companies are likely to see muted growth in both revenue and profit, both the technology and communication services sectors are expected to considerably outpace the broader market.

Projections indicate that six out of the seven companies in the “Magnificent 7” – NVIDIA, Amazon, Meta Platforms, Alphabet, Microsoft, and Apple – are anticipated to be the primary contributors to positive year‑over‑year earnings for the S&P 500 in Q4 2023. Collectively, these six companies are expected to demonstrate a 53.7% year‑over‑year earnings growth for the fourth quarter. If we exclude these six companies, the blended (combining actual and estimated results) earnings for the remaining 494 companies in the S&P 500 would show a decline of ‑10.5% for Q4 2023. Notably, the only company among the "Magnificent 7" not contributing positively to year‑over‑year earnings growth for the S&P 500 in Q4 2023 is Tesla.

The Magnificent 7 companies1 vs. S&P 493 index

1Seven stocks - Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla.

Shipping disruptions in the Red Sea

Attacks on ships in the Red Sea have caused challenges in global trade. The political instability in the Red Sea is forcing international shipping companies to undertake more expensive routes. That, in turn, is placing heightened pressure on businesses to reassess their supply chains. Shipping disruptions in the Red Sea may affect product prices, although not to the same extent as observed during the pandemic. Stakeholders are scrambling to adapt, though many companies report not yet feeling the effects. Tesla and Volvo Cars previously announced the suspension of some production in Europe due to a component shortage caused by numerous ships being rerouted around the southern tip of Africa. In contrast, BMW reassured that their factory supplies are secure, stating, "All lights are green", while Norwegian fertilizer giant Yara mentioned it was only mildly impacted by the transit challenges in the Red Sea.

Market view

The financial markets have started the year positively, with expectations for lower interest rates in the coming months. Overall, we continue to see economic growth, inflation, and the central banks as key drivers of financial markets in the foreseeable future. Nevertheless, some volatility and consolidation can be anticipated, given that much of the economy's positive news may have already been factored into market valuations.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.