Central bank actions impacting market sentiment | Luminor

Central bank actions impacting market sentiment

- US Federal Reserve (Fed) pushes pause on interest rate hikes

- ECB staying the course

- China's Central Bank's unexpected move

- Earnings trends will be key to watch for equity direction

As we assess the current market landscape, several key factors have influenced the recent market upswing, including a notable Q1 earnings season, decelerating inflation, growing optimism about a soft, non‑recessionary landing, the AI (Artificial Intelligence)‑powered tech rally, and the Fed approaching the end of its tightening cycle. These factors have played significant roles in driving the positive momentum. However, it is important to acknowledge that with much of the positive news already priced into the equity market, there is an increased vulnerability to potential disappointments. During June the developed markets stocks’ index MSCI World (EUR) has risen by 3.63% and the emerging markets stocks’ index MSCI Emerging Markets (EUR) has added 1.43%.

The US Federal Reserve introduces the idea of a "skip" meeting

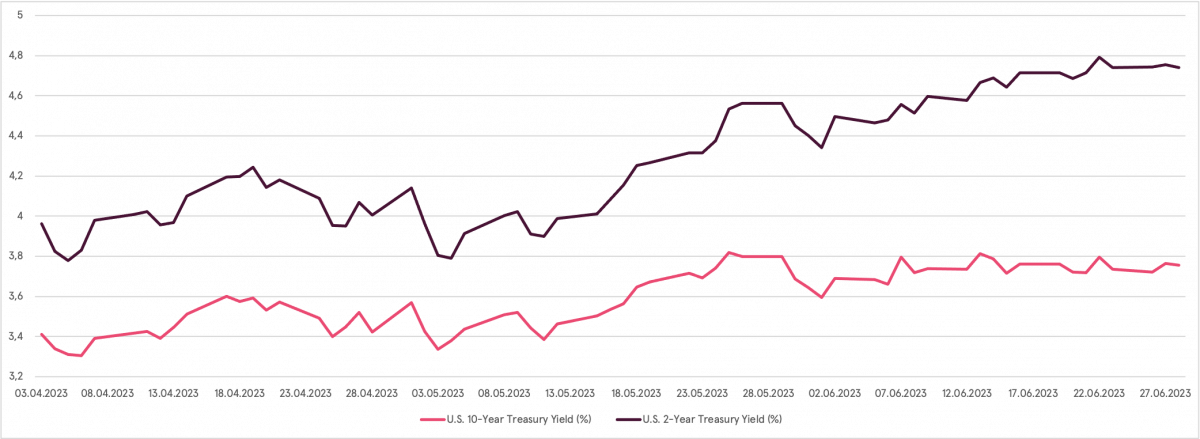

The US Federal Reserve paused its interest‑rate‑hiking cycle, keeping the Fed funds rate at 5.0%–5.25%, after 10 consecutive rate hikes. However, it indicated in its updated projections that a peak Fed funds rate could be around 5.6%, which implied perhaps two more 0.25% rate hikes ahead. This comes even as CPI and PPI (Consumer price index and Producer price index) inflation readings surprised to the downside. Nonetheless, in his comments Jerome Powell acknowledged that the Fed tightening thus far has put some downward pressure on growth and inflation, pointing to the tightening in bank‑lending conditions as well. Meanwhile, bond yields climbed higher after the Fed meeting, as markets priced in the potential for additional Fed rate hikes. The 2‑year Treasury yield moved higher by 0.10% to 4.68%, now nearly 1.0% above its recent lows in May.

U.S. Treasury yields climb higher as the Federal Reserve points to more rate hikes ahead

Source: Bloomberg L.P.

ECB tackles inflation with rate hike

Monetary policy was also in the spotlight on this side of the Atlantic, with the European Central Bank (ECB) announcing a 0.25% rate hike during its June meeting, bringing its main rate to a 22‑year high of 3.5%. This marked the eighth consecutive rate hike, despite the bloc entering a recession in early 2023, with both headline and core inflation rates persistently exceeding the ECB's 2% target. Additionally, the central bank has revised its inflation forecasts upwards while slightly reducing growth projections, particularly for the current and upcoming years. Meanwhile, during a news conference, President Lagarde stated that the ECB had more ground to cover and would likely continue raising rates in July. ECB officials have already implemented an unprecedented 400 basis point increase in rates over the past year, marking the fastest tightening pace in the history of the bank.

Surprise rate cut by China Central Bank to stimulate economy

China's central bank surprised economists and market participants by reducing a short‑term policy interest rate. This unexpected action reflects the increasing worry among officials about the country's slowing economic growth. “Policymakers are finally acknowledging the economic weakness,” said Michelle Lam, Greater China economist at Societe Generale. The reduction in interest rates was modest – a tenth of a percentage point for the country’s benchmark one‑year and five‑year interest rates for loans. However, since the majority of corporate lending and mortgages in the country are tied to these rates, the cuts could potentially impact the overall rate of economic growth to some extent. While the reduction in interest rates may provide a temporary boost to sentiment, economists say more needs to be done to boost confidence for businesses to invest.

Will earnings face a downturn or a steady course ahead?

The earnings recession that negatively affected the market for a significant period of the past year has started to stabilize, indicating that analysts were overly pessimistic. Factors such as the economy's resilience, cost‑cutting measures like layoffs, and disinflationary trends that improved profit margins, along with increasing enthusiasm surrounding AI, have helped prevent further decline in earnings. As a result, the S&P 500's projected earnings estimates, which had reached a low point of $226, have rebounded to approximately $232, reflecting an improved corporate profit outlook. This positive development has contributed to the broader trend of increased risk appetite in the markets observed over the month of June. Within a matter of weeks, we will enter the second‑quarter earnings season and closely observe whether companies can maintain these positive trends in the wake of more challenging consumer and economic headwinds.

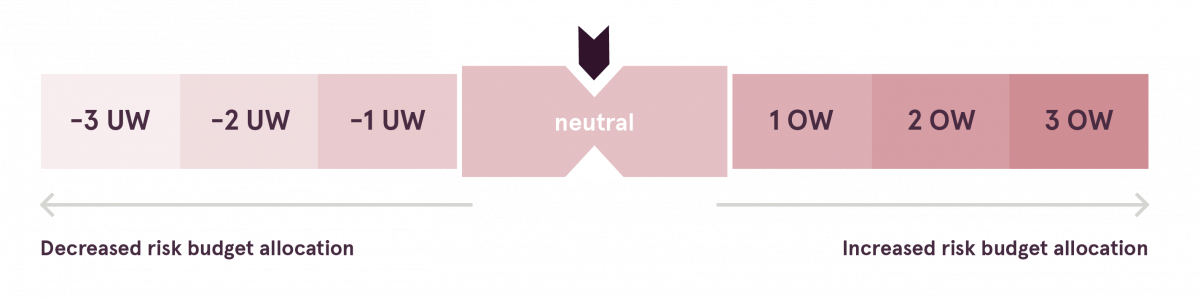

“House view” update

Our investment team remains committed to a neutral risk allocation considering the current market dynamics. We consider a range of both positive and negative factors in our decision‑making process. Factors such as decelerating inflation, the AI‑powered tech rally, and growing optimism about a soft, non‑recessionary landing contribute to the positive outlook. On the other hand, the restrictive monetary policy and macroeconomic uncertainty continue to rank high on our list of concerns. Taking all these factors into account, we believe maintaining a neutral risk allocation is justified.

Luminor House View

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.