Calm waters disrupted | Luminor

Calm waters disrupted

- Equity volatility increased

- Small-caps vs. large-caps

- Beyond the political noise

The market's spotlight expanded last month to include the evolving political landscape. However, the shift in the US presidential election matchup wasn't the only notable development; a significant rotation within the stock market also drew considerable attention. Stocks saw wide swings throughout the month, beginning with an early month rally that pushed U.S. markets to new highs, followed by a decline toward month-end, primarily driven by weakness in the tech sector. Investors concerned about the recent stock pullback are hoping the upcoming earnings season will provide a boost to their enthusiasm.

As a result, developed markets’ equities (measured by MSCI World index) have risen 0.79%, while emerging markets’ equities (measured by MSCI Emerging Market index) declined 0.66%. During the same period yields on bonds have decreased, with 10-year US Treasury bond yields declining to 4.03% from 4.41% a month ago, while German 10-year Treasury bond yields decreased to 2.3% from 2.49% a month ago.

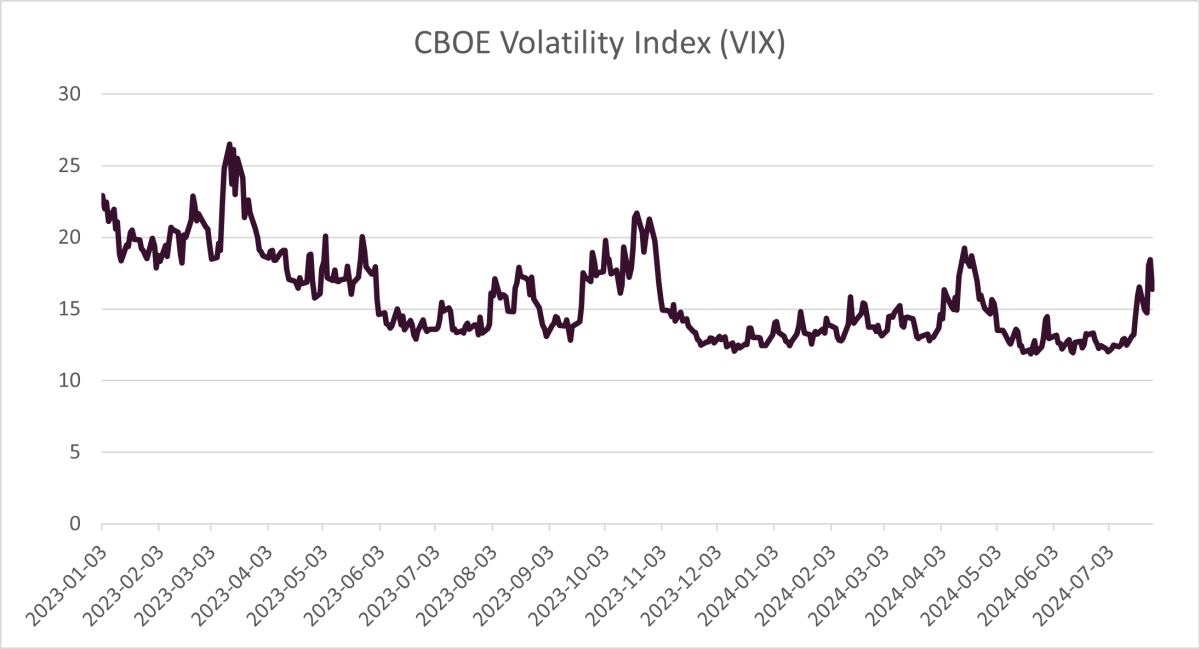

Equity volatility increased

The recent downturn in the stock market has made headlines and sparked some nervousness among investors. It's reasonable to anticipate that some weakness may persist as market participants navigate election uncertainties, upcoming quarterly earnings reports, and potential central bank actions influenced by the ongoing balance between high but decreasing inflation and positive but slowing economic growth. Meanwhile, the VIX Index1, commonly known as Wall Street’s “fear gauge,” has risen to its highest levels since April. This surge in the VIX reflects heightened investor concern, similar to when equity indexes experienced this year's first correction in April, marked by at least a 5% decline.

In July, equity market indexes displayed some weakness, but there are two key aspects to this pullback. First, the decline comes from an all-time high, with the stock market still up more than 13% year-to-date. Second, the dip is largely driven by weakness in big tech stocks, which have been among the significant outperformers this year. At this stage, this decline does not appear to be a broader market downturn. It may instead reflect the profit-taking activity in the stocks of the biggest gainers rather than being driven by new risks or concerns about the underlying fundamentals.

Source: Investing.com

Small-cap stocks surge amid market rotation

Last month saw a notable shift with a resurgence in small-cap stocks. After spending much of 2024 relatively stagnant, small-caps surged, with Russell 2000, a key benchmark for this market segment, notably outperformed, rising more than 10%. This outperformance suggests a potential shift in market leadership towards more economically sensitive investments, as the prospect of easier Fed policy boosts these segments. The second-half consensus earnings estimates for small-caps are healthy, but their realization will depend on the economy demonstrating resilience in the coming quarters. Conversely, signs of slowing growth or a less favorable stance from the Fed could hinder this progress. For context, small-caps rallied 27% in November and December of 2023 amid growing signs of economic resilience, but that rally dissipated as persistent inflation dashed hopes for a spring Fed rate cut. Sustained evidence of a soft landing will be crucial for maintaining this momentum.

Political violence during July

The major political events leading up to November’s presidential election have been nothing short of extraordinary. From Biden’s debate performance to Trump's guilty verdict and rise in the polls following the assassination attempt, this election is shaping up to be unprecedented. Despite these jarring events, the equity markets for the most part have remained mostly calm. Finally, in a surprising announcement, President Joe Biden stated that he will not seek reelection in November as the Democratic nominee, endorsing Vice President Kamala Harris for the nomination. This decision comes amid increasing pressure from Biden’s Democratic allies to step aside following the June debate. This latest twist in the political landscape adds potential uncertainty to the final outcome of the U.S. election. However, the stock markets reacted relatively calmly to the news, and this market response suggests that investors do not anticipate significant policy changes from the forthcoming Democratic nominee. Meanwhile, Donald Trump remains the favorite to win the election according to polls, though his odds have decreased following the recent developments.

Market view

Despite the flow of political news, we remain in generally early days of the presidential election process, significant developments and changes in the election process are still expected as these major events approach. While there may be shifts in polling and news ahead, most probably markets will continue to be driven by the fundamentals rather than the political headlines. We continue to see a macroeconomic environment where economic growth is cooling but remains positive, inflation appears to be easing, and the Fed looks poised to lower interest rates in the back half of the year. Regarding fundamentals, the markets will have to digest the upcoming corporate earnings reports. Healthy profit growth across various sectors could broaden market leadership in the coming months and potentially extend the current bull market.

1 The Cboe Volatility Index (VIX) is considered by many to be the world's premier barometer of equity market volatility. The VIX Index is based on real-time prices of options on the S&P 500 Index and is designed to reflect investors' consensus view of future (30-day) expected stock market volatility. The VIX Index is often referred to as the market's "fear gauge" (cboe.com).

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.