September arrives with a gust of wind | Luminor

September arrives with a gust of wind

- The oil price rally sparks inflation worries

- Yields reach new highs for the year

- Consumer is showing some signs of fatigue

This September has proven to be challenging for both the stock and the fixed income markets, as both have witnessed negative results. Investors find themselves contending with a multitude of conflicting factors. While stronger economic data and a tighter labor market offer the potential for a soft landing and an earnings recovery, they also contribute to persistent inflationary pressures and a Federal Reserve inclination to maintain higher rates for an extended period. Simultaneously, rising bond yields and a noticeable slowdown in economic growth in Europe and China are exerting a negative impact.

For the month of September, developed markets’ stock index MSCI World has retreated -1.9%, while emerging markets stocks’ index MSCI Emerging Markets has dropped -2.1%. Meanwhile, US bond yields have surged significantly, with 10‑year US Treasury bond yields rising to 4.62%, marking a 16‑year high (4.10% 1 month ago). Similarly, German 10‑year bond yields rose to 2.96%, up from 2.47% a month ago, as major central banks paused rate hikes but left the door open for more.

How big of a threat are rising oil prices?

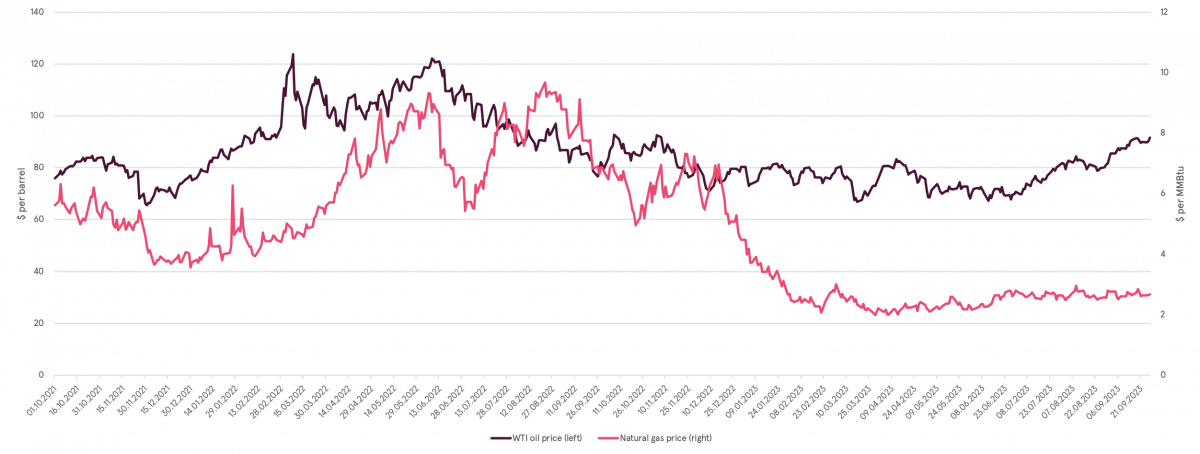

After averaging $75 for most of the year, WTI (West Texas intermediate) crude oil prices reached a 10‑month high of about $93 a barrel, but they are still well below last year's $123 peak. The main driver behind the recent surge has been production cuts from Saudi Arabia (the top oil exporter) and Russia, as both countries announced earlier this month that they will maintain the current lowered production through the end of the year. On the other hand, from a global‑demand perspective, sluggish growth in China, which is the biggest oil consumer, and a slowdown in European activity could prevent a more significant rise past the $100 mark.

Elevated energy prices generally act as a tax on the consumer. As households allocate a greater portion of their budget to gasoline expenses, they have less funds available for other expenditures. However, this situation can also help in controlling core inflation, as it may result in reduced demand for certain services. And unlike the surge in oil prices seen last year after the invasion of Ukraine, natural gas prices have remained stable, staying close to their three‑year lows. This stability is expected to offer ongoing relief in terms of utility costs.

Oil prices rose to 10‑month highs, but natural gas prices have not followed

Source: Bloomberg L.P.

10‑year yields hit 16‑year peak

Global Central banks warned against premature expectations of rate cuts, which pushed rates across the yield curve to multiyear highs. Among major central banks, none seem to be in a more demanding position than Christine Lagarde at the European Central Bank (ECB). The reason for this tough situation is that inflation remains stubbornly high in Europe, which triggered the ECB’s decision to hike rates a quarter point on September meeting ‑ its tenth straight meeting with a rate hike, despite the sluggish economy.

Meanwhile, in the U.S. markets, there’s still uncertainty about whether the Federal Reserve (Fed) is completely done. However, unlike Europe, the domestic economy in the U.S. remains resilient, and inflation is on a better trajectory than its European counterparts. Nevertheless, worries about a potential government shutdown have emerged, further putting the negative impact on sentiment.

As indicated in the headline, the main attention was on bond yields, which reached multiyear highs, as the Fed plans to keep interest rates higher for longer. The 10‑year yield approached 4.62%, marking its highest level since 2007, pressuring growth‑style investments and the technology heavy Nasdaq.

A cloud of uncertainty surrounds consumer spending

Consumer spending has demonstrated remarkable resilience. For a significant portion of the year, a strong job market, substantial wage increases, and surplus savings resulting from the pandemic have propelled spending, particularly in travel and leisure activities. However, these good times seem to be fading away. Despite a drop in inflation, consumers are increasingly exercising caution and selectivity in their spending patterns, a trend frequently emphasized during company earnings calls this summer.

Furthermore, with the slowing jobs’ growth (and with expectations of further weakness in the first half of 2024), the complete depletion of excess savings, the resumption of student loan repayments on October, climbing fuel prices, and rising borrowing costs, the outlook for both consumers and the broader economy is growing significantly more fragile.

Market view

In September, investment team has maintained its market positioning. The prevailing economic outlook suggests a somewhat cautious approach across various asset classes. Risk assets have largely adopted a 'wait‑and‑see' stance since the end of summer, resulting in an overall sentiment that leans slightly towards a 'risk‑off' posture. This shift can be attributed to pressures on consumption and tightening conditions in both the US and the EU.

Luminor House View

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.