Reduced uncertainties return investor optimism, but no clear skies there yet | Luminor

Reduced uncertainties return investor optimism, but no clear skies there yet

Darius Svidleras

Investment Portfolio Manager

- Supported by reduced political risks and increase in monetary stimulus, global equities updated new 2019 highs

- Risk of global economic recession still remains elevated, thus ongoing rally might not be sustainable despite investor optimism

- Forward guidance on earnings growth remains strong, but may be subject to reevaluation should the economic slowdown continue

Excluding the selloff in the first two trading days of October, when global equities dropped by almost 3%, the rest of the month was rather calm, allowing stocks to steadily rise in price, updating their 2019 highs with the onset of November, and in case of US indices even making new all-time high. Such positive dynamics was achieved due to mitigation of several major risks, which we also discussed in previous report.

First of all, trade negotiations resulted in successful outcome between USA and China. After Chinese vice premier Liu visited Trump in Washington, both countries agreed to reach preliminary deal. Written agreement is still to be developed and signed, but USA as a measure of good intention has already cancelled planned increase of tariffs on Chinese goods in October. Moreover, throughout the month representatives of both countries were reassuring investors that further progress in trade discussions is being made and written deal is almost finalized and is certain.

Another reason for modest optimism was linked to Brexit situation in Europe. Long story short, UK prime minister and EU leaders were able to agree to a deal, but UK parliament decided that more time is needed for them to fully understand the details of the new proposed bill to accept it, and thus Brexit deadline has to be moved once again. EU agreed to provide extension and move the new deadline to 31st of January 2020. Overall, similar to USA/China discussions, European leaders tried not to escalate situation around Brexit, sending message to the financial markets that the process of UK separation from EU would be tried to be made as smooth as possible.

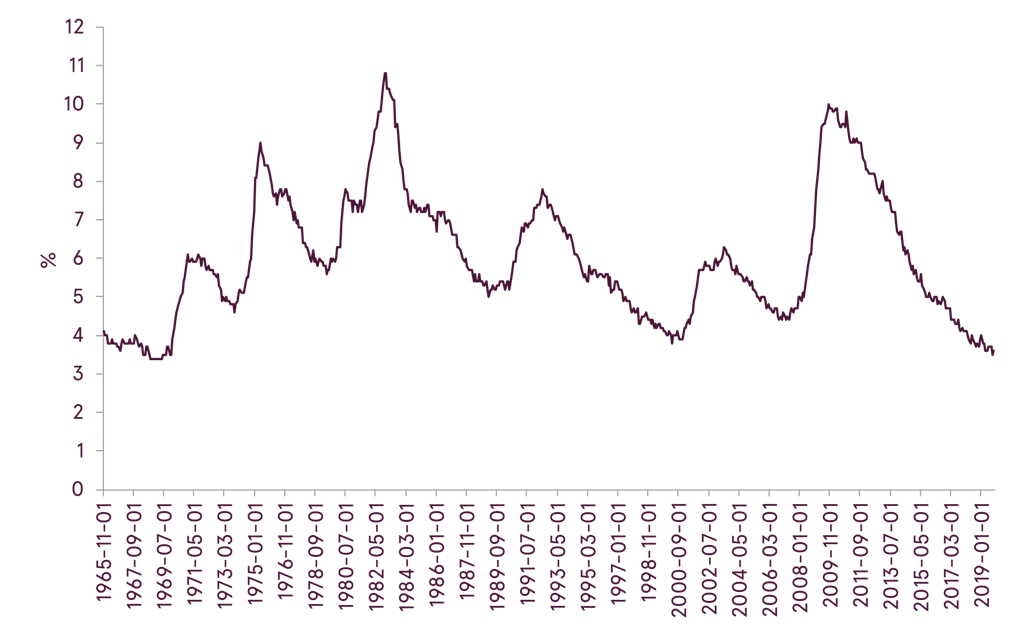

Also in October there was another round of major central bank meetings. In Eurozone there was no major change to existing monetary policy, as all attention was linked to the departure of Mario Draghi after his 8 year tenure as the ECB president. At the same time FED continued to reduce interest rate. With the third consequent cut to 1.75%, FED once again tried to ease financial conditions to prevent the US economy from slowing down. However, FED chairman Jerome Powell also indicated, that additional cuts are unlikely to happen in the foreseeable future, unless economic conditions would significantly deteriorate from current levels. In that regard, FED is likely referencing to data on employment which contrary to some other macroeconomic statistics still remains strong in USA. Specifically, unemployment rate in September was 3.5%, lowest reading in the last 50 years.

US unemployment rate

Source: Bloomberg

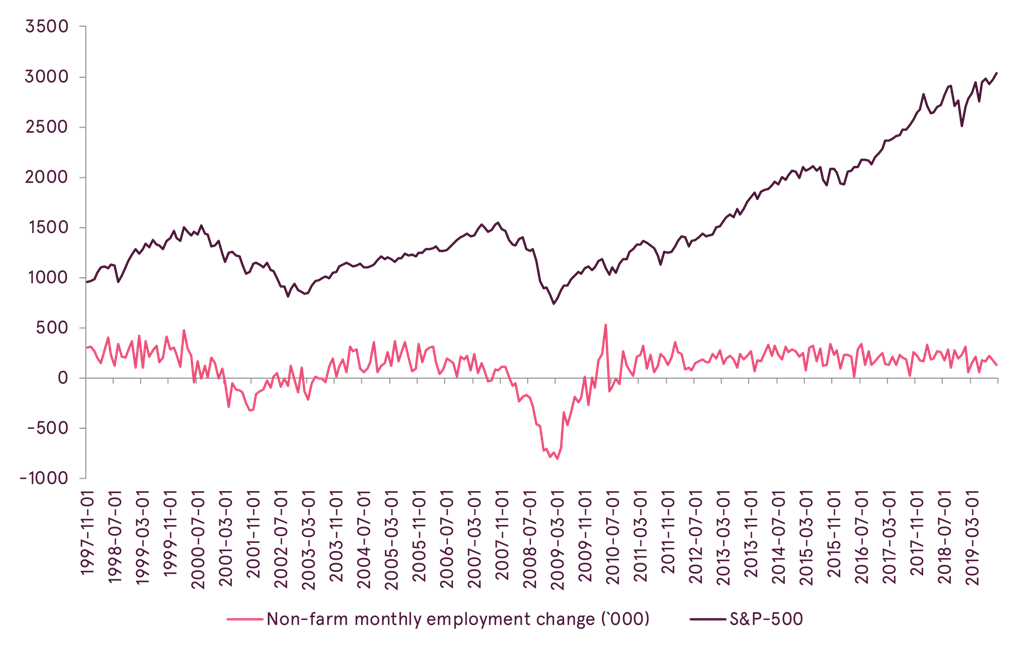

Indeed, historically start of two previous major bear markets and economic recessions coincided with first negative monthly change in number of employed people1 late in the US economic cycle. Since September 2010, US economy was capable to create additional jobs for every single month, and until this number would continue to remain positive, it is reasonable to expect that stock market would still have powder to rise higher, even if other macroeconomic data is showing some signs of weakness.

US monthly employment change vs S&P-500

Source: Bloomberg

Continuing discussion on USA, it is important also to mention relatively decent corporate financial reports for third quarter 2019. Based on already published data from 356 companies in S&P-500, their total corporate earnings declined by only 0.8%, while total revenue increased by 3.7% compared to last year2. While these numbers are far from being strong, the result is still quite solid given weakness in the global economy and trade uncertainty witnessed throughout this year. But what is more encouraging, analysts now believe that earnings growth may again become slightly positive next quarter, and as high as +10% in 2020, after some positive forecasts were provided by companies’ management.

Refinitiv earnings 2019-2020 projections

F – forecast

Source: Refinitiv

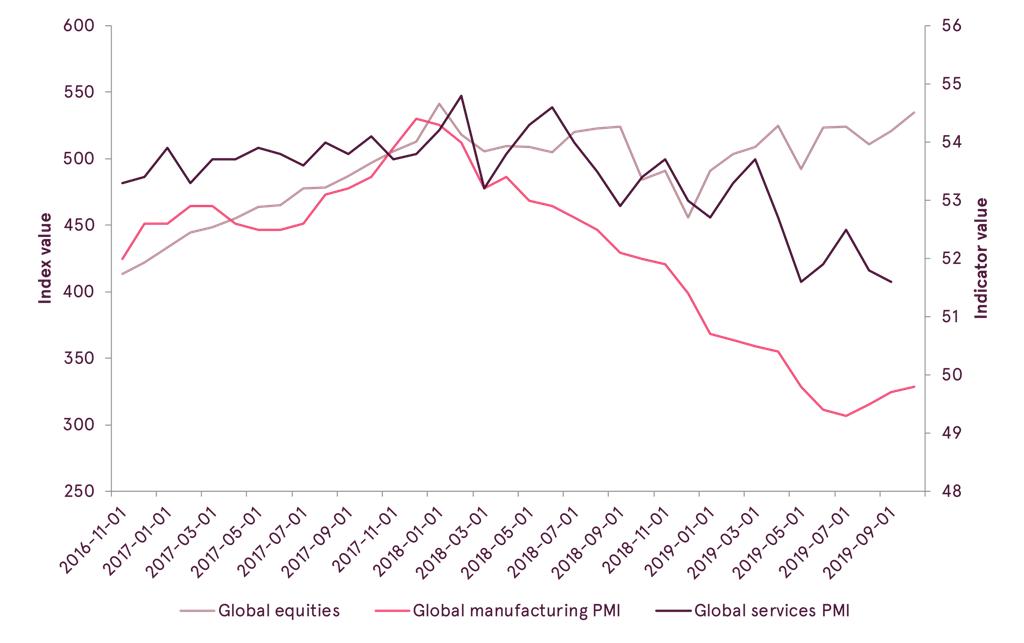

So there were certainly reasons for rising investor optimism by the start of November, with large number of financial pundits reasoning that equity prices should increase even higher in the upcoming months. While such statements may turn out to be true, we want to stress out that any sustainable increase in prices needs to be confirmed by improvement in economic indicators as well. And unfortunately we still see no such confirmation, as OECD leading indicators are still trending down. Moreover, if previously slowdown in economic activity was mostly linked to manufacturing impacted by weakness in global trade, currently we also see some disturbing trends in economic activity linked to services, which usually remain more resistant to external factors.

OECD total composite leading indicators vs global equities

Source: Bloomberg

Global manufacturing and services PMI vs MSCI ACWI

Source: Bloomberg

And even if we try to dig a little bit deeper in what appears to be truly positive data, such as aforementioned employment numbers in USA, we will find “red flags” there as well. Employment change is still positive, but growth is constantly getting weaker throughout the year, and in October it repeated the worst result since 2011. Or let us take Q3 reports, while US earnings were relatively fine, in Europe decline constituted 8.4% based on recent data, and this is concerning.

Growth in non-farm employment change (y-o-y)

Source: Bloomberg

Then let us return to the topic of trade negotiations. How many times this year we heard from the Trump administration about trade discussions going well and being in final stage, only to find out later that instead of promises tariffs were increased again. As there is still no written agreement, and both USA and China made it clear that first agreement would only resolve part of their mutual issues, further escalation should not be ruled out. As ridiculously as it may sound, one threatening tweet from Trump, and financial markets might become vulnerable once again.

Therefore, despite ongoing improvements, the risk of global recession still remains relatively high, and the possibility that equity markets would significantly drop in price, as it happened last year, is also not out of question. Nevertheless, there are several factors that point to a decent potential for stocks in the longer term. First, investor sentiment is far from extreme optimism and exuberance which is common for the market top. According to the American Association of Individual Investors 66% of investors are currently either neutral or bearish which is higher than historical average of 62%. Moreover, a significant decline in interest rates made equities more attractive relative to bonds, as stocks are still offering fairly strong earnings yield. As a result, possible volatility in the near term may provide good opportunities for the longer term investments.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.