October uncertainties require cautious stance in the market | Luminor

October uncertainties require cautious stance in the market

Darius Svidleras

Investment Portfolio Manager

- Equities rallied towards September central bank meetings, but continue to struggle afterwards

- Scheduled trade talks, Brexit deadline and start of earnings season – all indicate that October could be rather volatile month

- Unpredictability raises caution, so until there is progress in resolving prevailing uncertainties, global financial markets may experience significant volatility

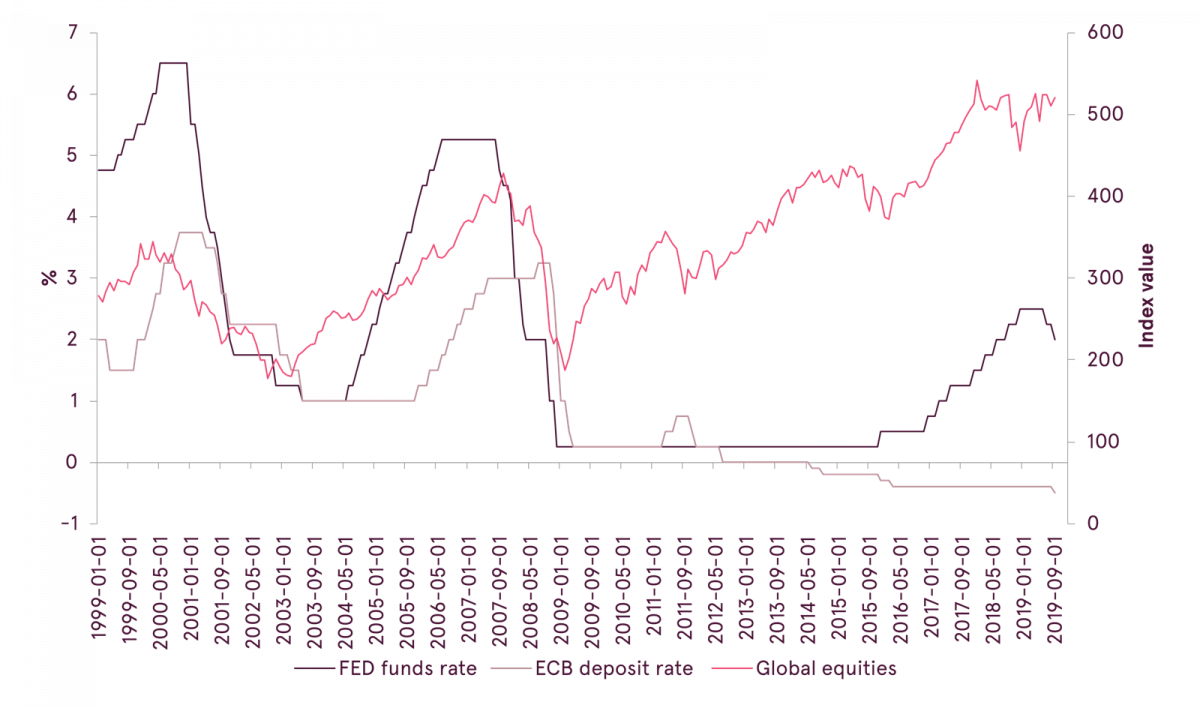

Driven by expectations of more monetary stimulus, global equities were steadily rising in first part of September, almost fully recovering losses experienced in early August; however, after ECB and especially after FED meetings dynamics started to shift towards downside once again.

Overall, central banks delivered what was expected from them. ECB reduced deposit facility rate from -0.4% to record value of -0.5%, and announced new round of quantitative easing at EUR 20 billion per month starting from November. FED cut interest rate by another 0.25% to 2%, and Chairman Powell hinted that if needed, Central bank would be ready to increase balance sheet and resume asset purchases. As markets have already increased by ~7% from August lows towards the meetings, and no other major unambiguously bullish events were yet to be seen on the horizon, investors decided that it was good time to start taking profits in second part of September and going into October.

Main interest rates and performance of global equities

Source: Bloomberg

All country world index (in USD)

Source: Bloomberg

But predicting market movement in the upcoming weeks and possibly until the end of the year becomes increasingly complicated task right now. There are several major catalysts with unpredictable outcomes expected to happen in October, and equities reaction might vary from strong upsurge to severe correction. So let us review each of these factors.

First and probably most important catalyst that is likely to move the markets this month is linked to trade negotiations between USA and China. Both countries agreed to meet on 10-11 October in Washington, few days before US tariffs on $250 billion of Chinese goods would be raised from 25% to 30%. Though it is impossible to predict, how ongoing conflict would resolve, nevertheless, if both countries are really willing to reach an agreement (at least preliminary), it would be favorable to do it this month without another postponement.

Key reason is that trade conflict continues to remain significant hurdle for a potential recovery in the global economy. Tariffs tend to increase prices and reduce demand for the goods, while businesses, engaged in international trade, cannot undertake new investments and make solid expansionary plans in such uncertain protectionist environment. If global slowdown, influenced by trade war, in the end would transform to full scale economic recession, both USA and China are likely to lose much more than what they are expecting to win with the tariffs. As time is ticking, some sort of compromise in October from USA and China would be very constructive, but if no agreement is reached once again, move down in equities stronger than in May or early August is certainly possible.

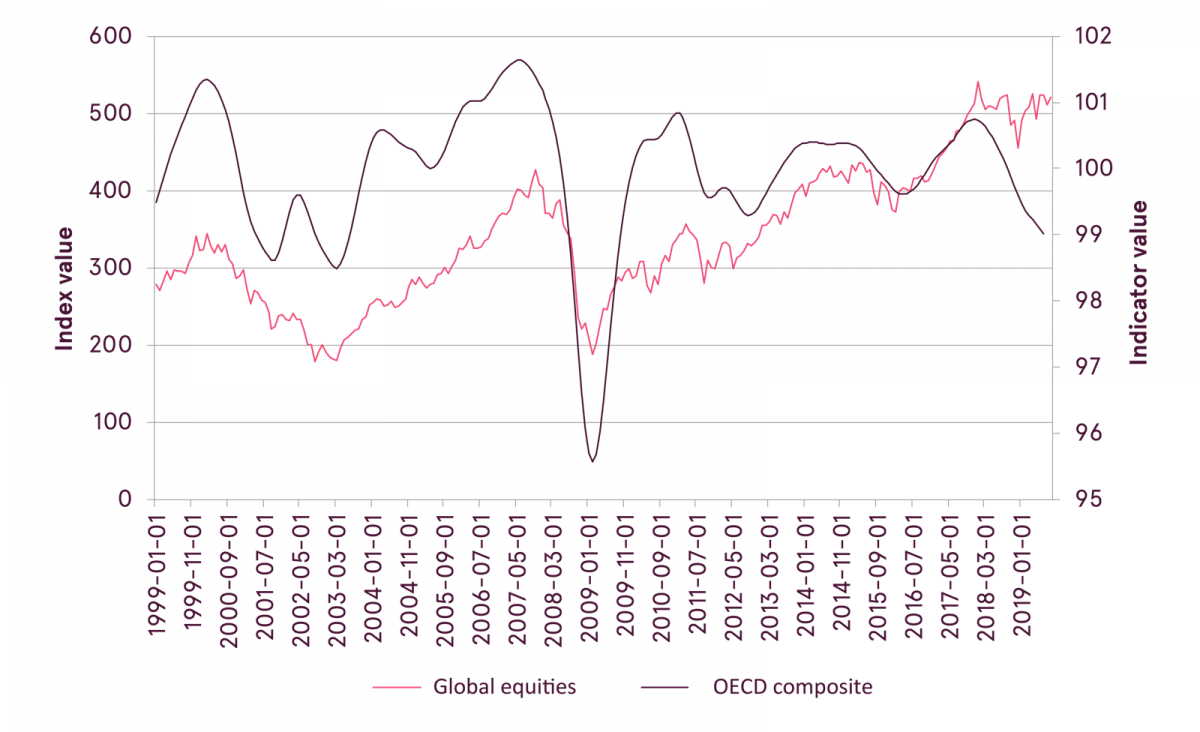

OECD total composite leading indicators vs global equities

Source: Bloomberg

Next issue that is again becoming important this month is Brexit; specifically, on 31st October UK is required to leave European Union. If this deadline is not prolonged, and by that time countries will not be able to reach some smooth agreement on the withdrawal, overnight UK would be removed from EU single market and lose all the benefits of being one of the EU members. It would also likely lead to additional taxes and tariffs on UK goods coming to Europe and other potential negative consequences. Again, it is hard to measure exact outcomes, but if there is “no-deal” Brexit or deadline is prolonged, adverse impact on both EU and UK economies as well as on financial markets should be expected; and contrary is true, if some deal is reached and there is more certainty in the situation once again.

In addition, in October majority of companies will release their earnings for third quarter of 2019. Previous results throughout the year turned out to be rather resilient to macroeconomic fragility, and it would be really important for results to continue showing relative strength. Otherwise, investors might realize that future earnings are likely to decrease and thus equities should be valued lower. Selloff would follow then.

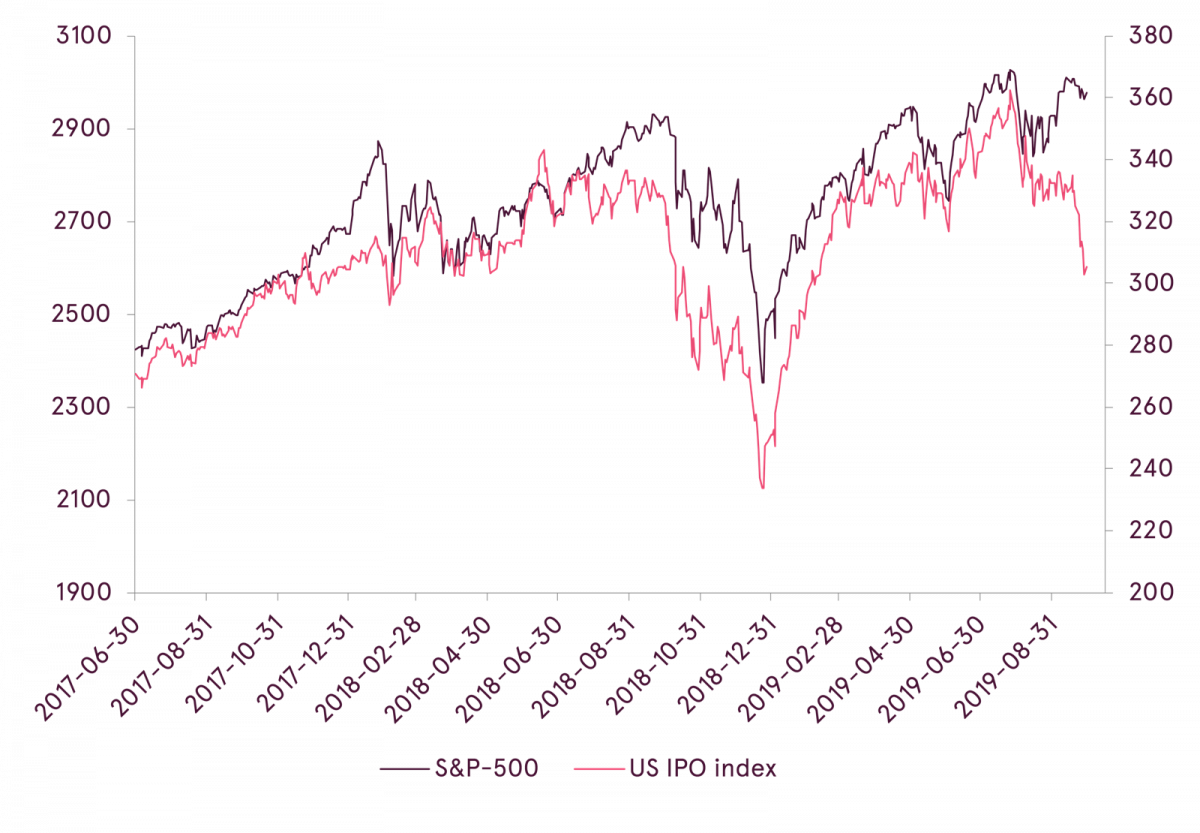

Speaking of valuation, one more subject is worth mentioning. Failed IPO of WeWork, startup which was valued at around $47 billion in January based on private investment from SoftBank, and which is now considered to be worth only around $10 billion after financial statements in preparation to IPO were revealed, is raising more serious question - is market correctly estimating value of recently listed technology start-ups and value of fast growing, but yet unprofitable companies in general. In September, significant divergence was observed between S&P-500 and index of recent IPO stocks, and this casts some additional concerns about the health of the market.

US IPO index vs S&P-500

Source: Bloomberg

However in the context of the current low yield environment it makes sense to look at the relative valuation between equities and bonds. One way to compare these asset classes is to look at equity dividend yield versus the bond yield, as this is the regular income that investors in these assets would receive if prices are kept constant. Although normally dividend yields are lower than long term bond yields, currently in most of the major regions, except emerging markets, equities are paying higher dividends than the yield on the 10-year bonds. From this point of view equities look more attractive than bonds. Still, investors should be aware that in case the economy continues slowing, corporate earnings and dividends may be at risk of significant decline.

Dividend yield vs 10-year bond yield

| Region | Dividend Yield (%) | 10-Year Government Bond Yield (%) |

|---|---|---|

| All Country World | 3,21 | 1,34 |

| Japan | 2,48 | -0,21 |

| Emerging Markets | 3,23 | 4,02 |

| Europe | 3,82 | -0,26 |

| United States | 1,95 | 1,68 |

Source: Bloomberg

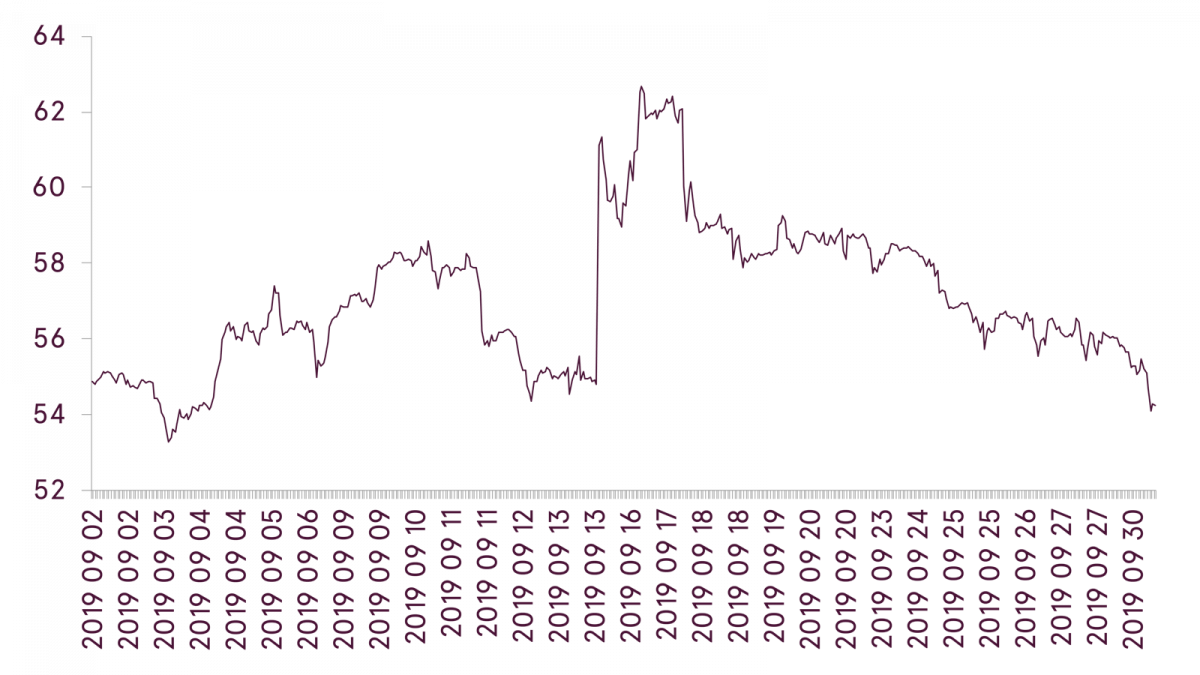

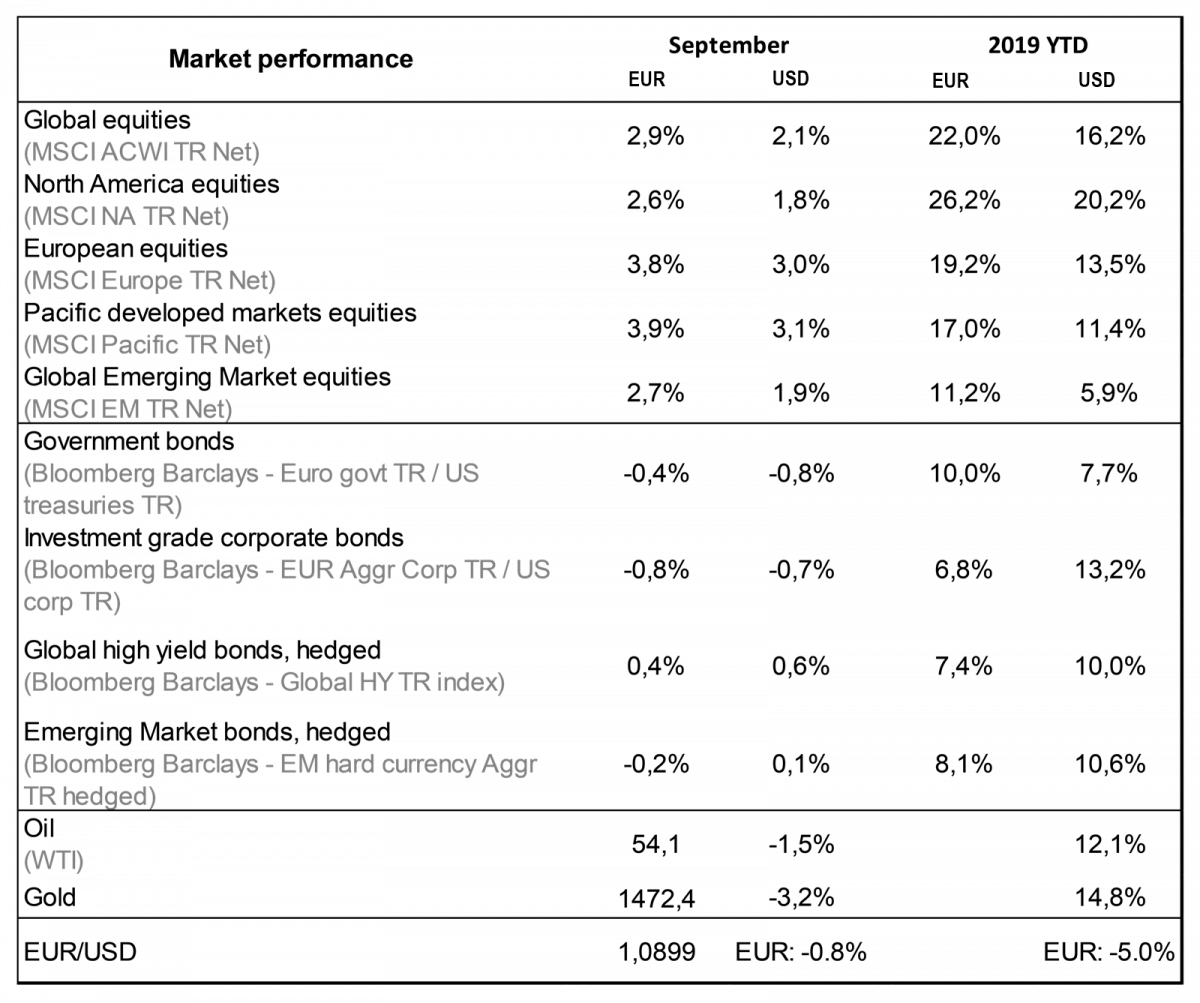

In other news, we witnessed temporary oil price shock in September, as oil fields of Saudi Arabian national petroleum company were attacked by the drones, and price of oil jumped by as much as 15% in one day. Major concern, is that Iran stands behind the attack, and thus, it makes major conflict or even war between two dominant Arabic powers quite realistic. So far Saudi Arabia is trying not to escalate the conflict, helping oil prices actually to drop in September. This is encouraging, as high price of oil is one of the least needed developments right now given rising risk of economic recession.

Crude oil (WTI) price chart in September

Source: Bloomberg

Summing up, by the end of September over 80% of global central banks have lowered interest rate as their last move. As a result, global monetary policy is very accommodative, which historically has supported both the financial markets and the economy. Nevertheless major political and geopolitical uncertainties have not receded. Such uncertainties make long term planning complicated, which hurts long term corporate growth and makes investors cautious and more reluctant to invest. Therefore until there is progress in resolving those uncertainties, global financial markets may experience significant volatility.

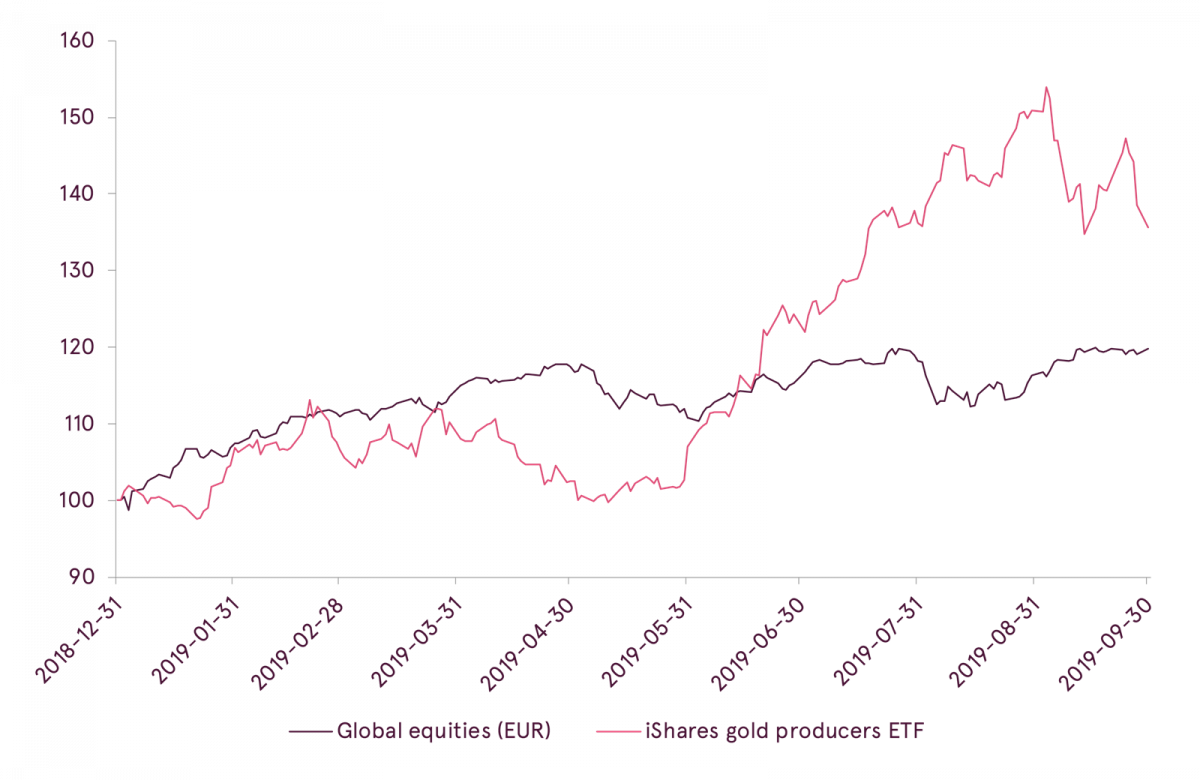

Performance of selected assets in EUR (year to date)

Source: Bloomberg

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.