November shines bright | Luminor

November shines bright

- November stock market rally

- Progress on inflation reduction continues

- Retailers put to the test

- Japan’s comeback

There's nothing quite like a winning streak spanning several consecutive days to shift the market narrative. This month, stocks have swiftly transitioned from a correction to a comeback, with major stock indexes now poised to challenge previous highs reached earlier in the year. Throughout the month, it appears that economic data are striking the right balance - neither too hot nor too cold, helping stocks reach a two‑month high and placing the October correction behind us.

As a result, developed markets’ stock index MSCI World has experienced 5.96% increase, while emerging markets stocks’ index MSCI Emerging Markets has risen by 4.63%. Meanwhile, US bond yields have decreased significantly, with 10‑year US Treasury bond yields dropping to 4.3% (4.93% 1 month ago). Similarly, German 10‑year bond yields decreased to 2.45%, down from 2.83% a month ago – both reflecting lower expectations for high interest rates in the future.

Expectations for a Fed (the Federal Reserve System) pause fuel November rally

A significant factor behind the rise in both stock and bond markets this November is that the easing inflation pressures, together with signs of a cooling labor market, increase confidence that the Fed is likely done hiking rates. Following the lowest core inflation reading in over two years, markets quickly adjusted by pricing out the rate hike in December and adjusting to reflect an earlier start to rate cuts.

The 2‑year Treasury yield is now below 5.0%, while the 10‑year yield declined below 4.4%, the lowest since September. It is possible that last month's surge in rates might have marked the peak for this cycle. Policymakers will likely push back against aggressive expectations for Fed easing, so there is a limit to how much and how fast yields can fall from here.

Progress on inflation reduction continues

Following a brief increase in late summer, inflation resumed its decline in October. The headline consumer price index (CPI) in the US was unchanged last month, with the annual rate falling from 3.7% to 3.2%, helped by a sizable drop in petrol prices. Oil prices have experienced a 17% decrease from their peak in September and probably will continue to be a downside factor on the upcoming month's data. Core CPI (excluding food and energy), which is considered a more accurate gauge of the underlying trend, also decreased from 4.1% to 4.0%. Despite remaining above the Fed's target, this marked the lowest reading in two years. Additionally, disinflation is also in full force in the Eurozone. Headline Year‑on‑Year inflation was confirmed at 2.9% in October, matching the initial estimate and down from 4.3% in September.

Adapting to consumer trends

In the face of economic pressures and inflationary environment, there has been a lot of concern about the pace of consumer discretionary spending in the US. Just how deep those concerns went could be evidenced by the stock performance of one of the largest retailers in the US – Target Corporation. Having halved since the retail heyday during the Covid pandemic, Target Corporation stock had lost further 30% this year at least partially thanks to the concerns over the consumer spending strength mentioned above.

Therefore, the recent earnings’ announcement of the better‑than‑expected sales figures and higher‑than‑expected confidence in the upcoming holiday shopping season could serve as an optimistic version of the canary in the mine not just for this particular retailer, but for the broader consumer discretionary spending trend in the US. So as to illustrate the potential of the positive surprise in the US consumer story, the investors have bided up the price of Target Corporation shares by 17% in a single trading session right after the news.

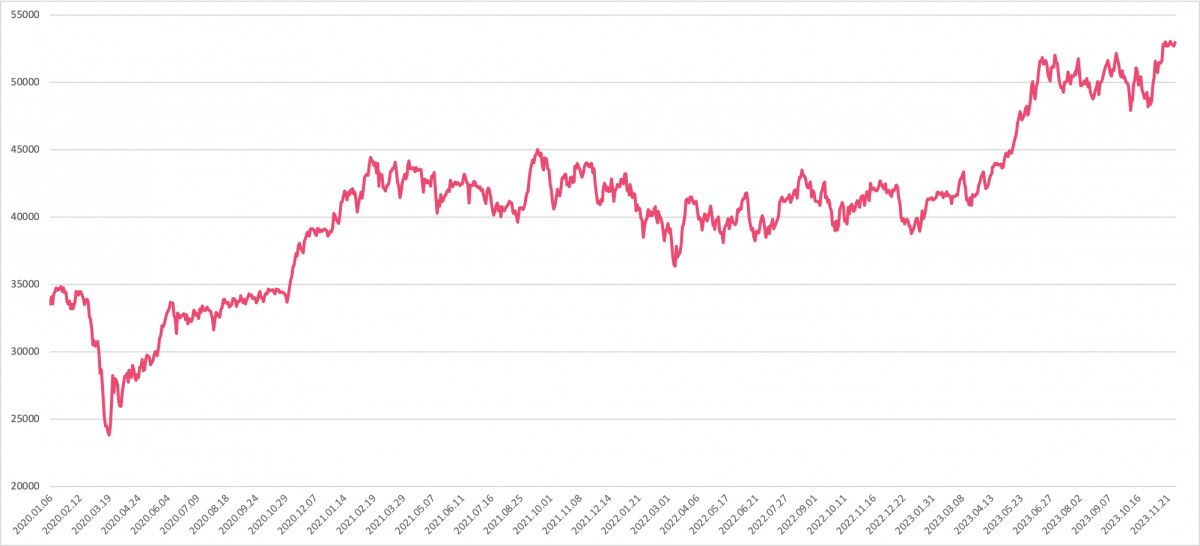

Japan’s comeback

For three decades, Japan's economy stayed stagnant, faced by a combination of low growth, low inflation, and low interest rates, but now Japanese stock indices are currently enjoying their highest levels in decades (measured in JPY), signaling a period of positive economic growth. At least a partial explanation lies in the historically low value of Japanese yen versus other major currencies, making exports‑reliant Japanese companies more attractive. However, this upswing is fueled by other factors, too, namely a robust macroeconomic environment, a break from years of deflation, as well as international interest reflected by rising foreign investments. A crucial catalyst for this optimistic trend is the ongoing corporate governance reform in Japan, which is focused on increasing the attractiveness of Japanese businesses to outside investments. While it's uncertain whether this positive momentum will lead to a permanent shift in the economic landscape, the overall outlook for Japan is notably brighter than in the past. Should the witnessed trends continue, this could potentially suggest a constructive opportunity for further diversification of the portfolios.

Nikkei 225 Total Return EUR hedged Index

Source: Bloomberg L.P.

Market view

Looking ahead, markets could be further kept down by the concerns over slowing economic growth, heightened geopolitical risks, and the repercussions of tighter financial conditions emerging. Despite these challenges, a potential shift in market dynamics towards a more sustained recovery is also possible in the coming future. This transition supports our largely neutral approach amid the current uncertainties. On the bright side, higher interest rates have made Fixed income part of the portfolios more appealing, especially if things stay uncertain and the economic activity gets slower from the current levels.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.