The great rate hangover | Luminor

The great rate hangover

- Stocks continue rising while bonds take a breather

- Interest rate cut expectations held back

- Chinese economic woes continue

- The resurge of India

Financial markets took largely diverging paths during the last month, as global stocks continued their march forward, while bond prices somewhat retreated on the scaled‑back interest rate cut expectations. One of the major catalysts for such market dynamics was mostly resilient macroeconomic data from major regions, ongoing excitement about the artificial intelligence (AI) business case, as well as the dominance of companies perceived to be related to AI in the US stock market.

As a result, the developed markets’ stock index MSCI World has increased by 4.1%, while the emerging markets stocks’ index MSCI Emerging Markets has jumped by 4.6%. During the same period yields on bonds have increased slightly, with 10‑year US Treasury bond yields rising to 4.25% (compared to 4% 1 month ago) and German 10‑year bond yields increasing to 2.41%, up from 2,17% a month ago.

Interest rate expectations rolled forward – bonds retreat

During the final months of 2023, a substantial part of market participants were expecting the first interest rate cut to take place as soon as March 2024, thanks to rapidly decreasing inflation, resilient yet subdued economic activity, and some encouraging remarks from the central banks themselves – first and foremost, the Federal Reserve (FED). So far, the culmination of such consensus has peaked in the final days of 2023. That narrative with the arrival of 2024 has been taken slightly off the aggressive track lately, as the multiple data points have shown more bustling economic activity than previously expected. Interestingly, the inflation figures in recent months have come out slightly higher than expected, too. Even if it’s down to technical reasons (e.g. the timing of fiscal measures), it appears to be contributing to a timely consolidation in the otherwise aggressive bonds’ rally since November. Even though it is likely that the rates have already reached their peak, central banks will most likely stay cautious with their further guidance and will be eager to wait for the data to confirm future moves.

China’s woes continue

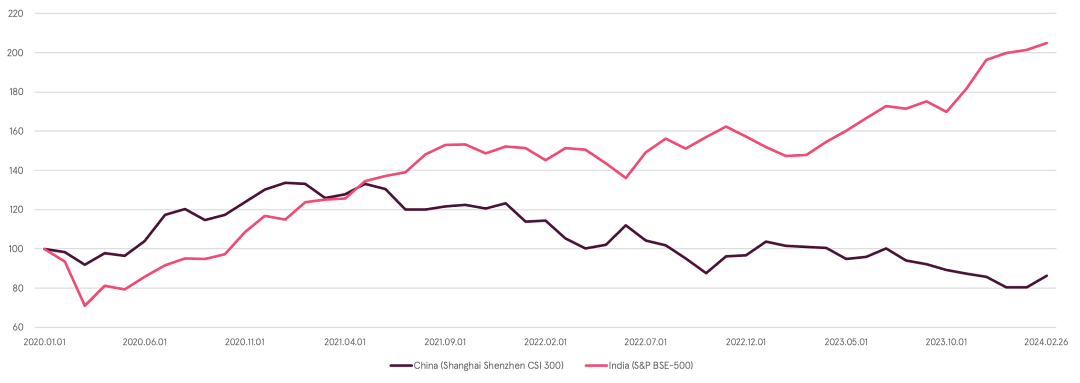

As millions of Chinese have been bracing for the Lunar New Year celebrations in February, investors in the stock market of the second‑largest economy in the world had little to celebrate this year. During the last few years investors in Chinese equities have had to endure the zero‑COVID policy‑induced slow GDP growth, regulatory crackdown on the prominent private Chinese businesses and individuals, the ongoing real‑estate bubble saga, and the over‑arching background of increased geopolitical risks, thanks to increased competition with the US and escalated rhetoric from the Chinese leaders towards Taiwan. This troublesome cocktail has given multiple reasons for market bears to push down the value of the CSI 300 index (see Chart) significantly, while the rest of the world has largely stayed bullish. February was noted by the court ruling that Evergrande – the second largest real estate developer in the country – should go into liquidation, as no success in debt restructuring talks has been achieved. Chinese stocks remain relatively cheap when compared to their peers, but investors will most likely be overly curious to see the next moves how the country will navigate the multiple challenges it faces before coming back.

Chinese and Indian stock market returns since 2020, %

Source: Investing.com

India roars back

Just as China has been facing its own challenges, another emerging markets star – India – appears to attract have attracted increased investor attention, lately. The country has not only recently overtaken China as the most populous country in the world (with a population of 1,4 bn set to rise further vs the expected decline in the Chinese population). India’s economic growth appears to be charging forward, too, as the economy is expected by OECD to showcase the largest economic growth among the major countries (6,2% and 6,5% in 2024 and 2025, respectively). As the country seems to be finally putting itself firmly in the global supply chains and heavily investing in the much‑needed infrastructure, some analysts are expecting India to become the third‑largest economy by 2027, overtaking Japan and Germany along the way. Finally, worn down by the geopolitical drama of the Chinese market, investors appear to appreciate India as a “Western‑friendly” emerging market alternative with jubilant economic activity to bank on. On the other hand, excited investors have pushed up the valuations of Indian equities rather high quite quickly, recently (see Chart). Hence, it offers investors the long‑forgotten excitement about the emerging market economy with high valuations and many potential pullbacks along the road in the future.

Market view

As the financial markets are pondering on their aggressive rate cut expectations, some asset classes (notably, bonds) are taking a breather before setting a further trend. The prevailing narrative of the “soft landing” seems to be offering support to continued strength in equity prices along with the hope that central banks will be coming back to concrete plans on interest rate reductions later this year.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.