Financial markets drift higher amid increased volatility | Luminor

Financial markets drift higher amid increased volatility

- ECB changed inflation target to allow inflation to overshoot its 2% target

- Prices in US are climbing higher, but markets still believe that inflation is transitory

Although we expected July to be quite noneventful month, policymakers and central banks announced market moving news, which could have a long-term impact. Moreover, in July, markets were spooked by the spread of the COVID-19 Delta variant, which could force governments to reintroduce restrictions or even lockdowns. Hence, most indexes had several sharp pullbacks during the month. However, every time a dip-buying trend prevailed, as investors rushed in to buy stocks.

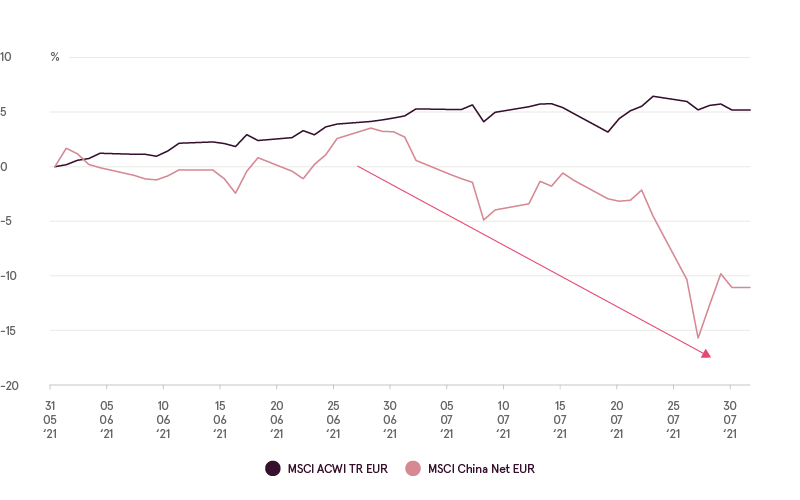

Asian stocks suffered big losses, as crackdown on Chinese companies intensified. Last month, country officials launched a data-related cybersecurity investigation into the ride-hailing company Didi Global soon after it raised USD4.4 billion in a New York IPO. Later, Chinese authorities imposed substantial limitations on the booming private education and tutoring sector. After onslaught of rules that limit growth and, in some cases, decimate entire business models, investors reevaluated the dangers of regulatory risk and started to cut exposure to such companies. Moreover, the stock rout deepened, as Chinese exporters were hit by rising costs and continuing supply chain disruptions amid shipping container shortage.

World and China equity indexes

Source: Bloomberg Finance L.P.

Central banks are starting to hint about the end of massive stimulus, which was introduced during COVID-19 lockdowns to support the economy. Rising prices of goods and services could provoke the European Central Bank (ECB) and the Federal Reserve (FED) to take measures to control inflation. Central bank governors understand that any hint of tapering could provoke sharp correction in the markets and their communication is very subtle.

After the 18-month strategy review, the ECB announced that they set the inflation target at 2% in the medium term. By doing so, they dropped their previous formulation “below but close to 2%”. The ECB made no specific reference to tolerating an inflation overshoot, but the ECB president Christine Lagarde acknowledged, that inflation could overshoot the target. She also mentioned, that the current ECB’s EUR1.85 trillion bond buying program is expected to last until March 2022 and afterwards it could be transitioned to a new format. The ECB said that current risks to growth are seen as “broadly balanced”, rather than tilted to the downside.

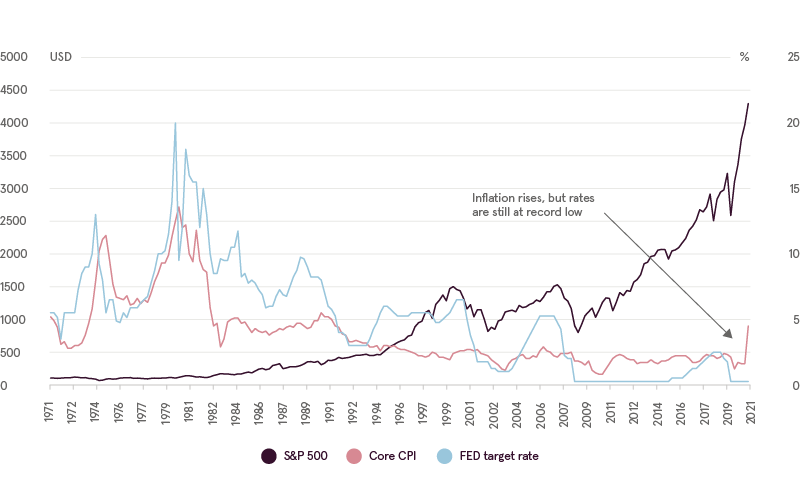

Prices for goods and services paid by US consumers surged in June the most since 2008, topping forecasts and testing the FED’s commitment to support the economy. Core CPI, a widely tracked US inflation measure, which excludes volatile components, rose 4.5% year on year in June 2021, the largest advance since November 1991. Nonetheless, investors’ reaction shows, that market participants still believe the FED prediction, that inflation overshoot is a temporary phenomenon.

Inflation, Fed target rate and S&P 500

Source: Bloomberg Finance L.P.

Currently, we see a mix of positive and negative factors, which influence the markets. For example, second quarter corporate financial results positively impacted equity indexes as most companies were able to beat forecasts. At the time of writing this overview, 87% of S&P 500 index companies announced estimates beating earnings, according to Bloomberg. Also, the initial market participant reaction to the spread of the COVID-19 Delta variant was quickly reversed, as vaccination rates are going up and the threat of a full lockdown does not seem that probable.

On the other hand, we still observe deterioration of market breadth indicators. For example, the percentage of S&P 500 stocks above their respective 50-day moving average (MA) decreased from almost 85% to below 50% of index constituents from the end of April to the end of last month. Moreover, the same tendency is also present in the World index (MSCI ACWI). At the end of July, less than half constituents of MSCI ACWI were above 50-day MA, while several months ago, more than 60% of constituents were above. This indicates that, “beneath the surface”, the market could be weakening.

In addition, increased tax burden is another long-term risk to IT giants and other multinational companies. The G20 finance ministers – who represent 19 countries with the largest and fastest-growing economies, as well as the European Union – backed a plan, which will see multinational companies pay a minimum global corporate tax rate of 15% around the world. The plan to battle tax avoidance is likely to affect companies like Amazon, Facebook, Google, and others.