As expected, not so much | Luminor

As expected, not so much

- Macron shocks the markets

- Indian elections come unexpected

- ECB lowers the interest rates

- Inflation in the US cools, interest rate cuts still uncertain

The month of June has turned out to be the month of quite a multiple amount of events that could shape the global economy and the financial markets for the foreseeable future. On one hand, the investors have finally got to taste the long‑expected news on central banks globally taking first steps towards reducing interest rates. On the other, the elections’ – busy year produced some unexpected results and outcomes, which in turn are substantially increasing the volatility in the market.

As a result, developed markets’ equities (measured by MSCI World index) have risen 1.9%, while emerging markets’ equities (measured by MSCI Emerging Market index) gained 3.55%. During the same period yields on bonds have decreased slightly, with 10‑year US Treasury bond yields declining to 4.41% from 4.5% a month ago, while German 10‑year Treasury bond yields decreased to 2.49% from 2.65% a month ago.

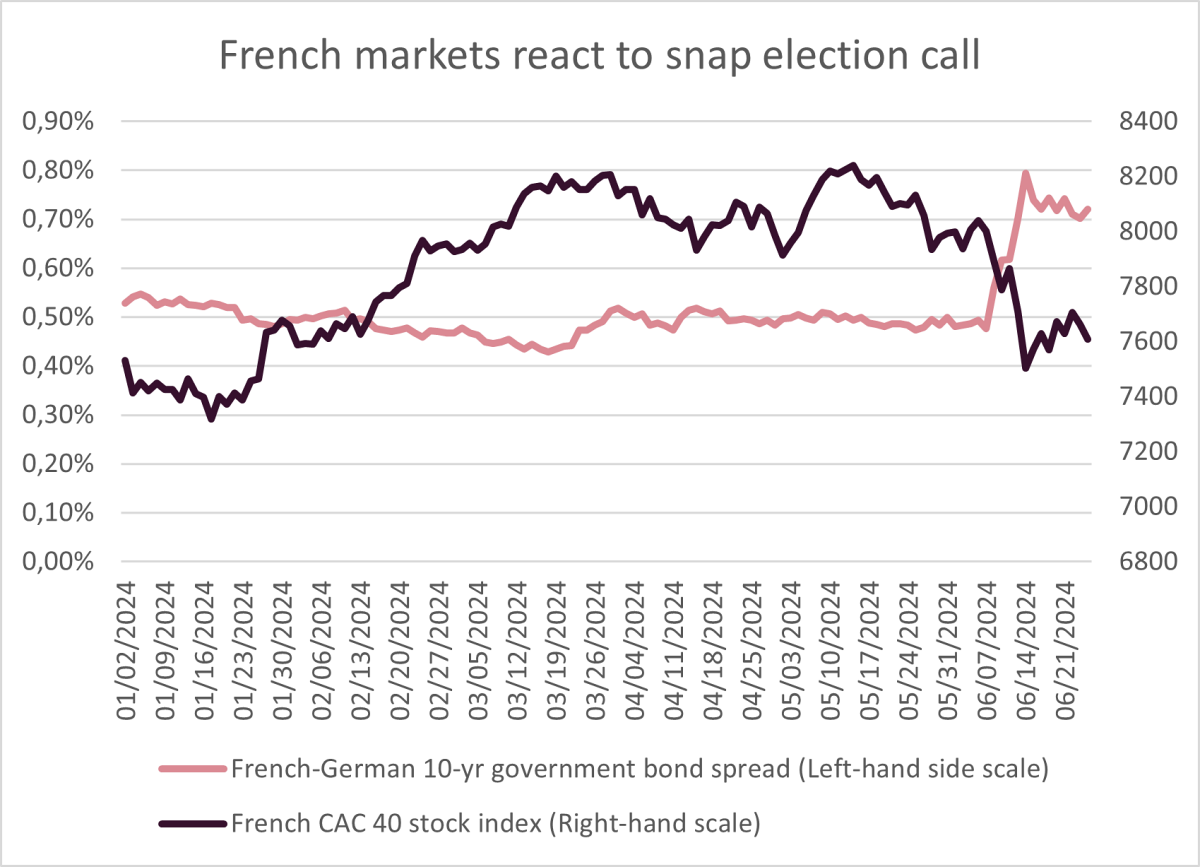

Macron surprises the markets

The European parliament elections that took place in mid‑June all over the continent has delivered the results that many polls had been suggesting for quite some time. In many cases, the mainstream incumbent parties and green‑agenda focused political movements have seen their popularity decrease, while parties on the right side of the political spectrum have largely gained additional seats in many countries. France was no exception in this trend, as the French president Emmanuel Macron’s centrist alliance ceded seats for the benefit of its competitors, especially the Rassemblement National party, led by long‑standing far right Marine Le Pen. In response, president Macron has unexpectedly called early parliament elections, thus unleashing the wave of uncertainty throughout the markets, as preliminary polls suggest Macron’s alliance could be facing a wipeout and the competing political agenda could potentially put France in fiscal jeopardy. As the markets got spooked by French snap elections, French bonds’ spreads over their German counterparts have increased from 0.50% to 0.80%, while stock market index CAC 40 dropped 6.23%, dragging down EUR/USD together with it.

Source: investing.com

Not so Modi in India

On the other side of the world, India has witnessed the outcome of the largest parliamentary elections in the world taking place over the course of weeks and getting finalized in the early days of June, only. Contrary to the many expectations of market participants, the Bharatiya Janata Party (BJP) led by Prime Minister Narendra Modi, has not only gained new seats in the election, but lost the parliamentary majority, which means that once‑dominant BJP will have to rely on its coalition partners to continue governing the country – something that India has not experienced since 2014. As BJP has been widely acclaimed for the impressive progress Indian economy and the stock market has been going through, the change in the highest ranks has instantly scared some investors running for the exits. As a result, the Indian equities’ index SENSEX has dropped up to 6% in a single session, before recovering all of the lost ground in the following sessions. Apparently, the leading emerging markets’ star India is bound to witness the change in the government, soon, but the optimists are still plenty on the story.

Interest rate cut, finally

On the central bank and monetary policy front the investors could witness some long‑waited decisions and trends finally unfolding, even though the shape and form may not be exactly what market participants had been expecting. European Central Bank (ECB) reduced the base interest rates by 0.25% in a widely expected move, although it remains highly uncertain, just how quick the central bank may be in the foreseeable future with follow‑on interest rate cuts. Substantial portion of analysts are suspecting ECB to stay wary of starting the full‑fledged new interest rate cut cycle before their American colleagues from the Federal Reserve (FED) join them. In the meantime, FED has been constrained in their ability to reduce the rates on the back of resilient economic activity and buoyant inflation in the US. Therefore, the fact that the inflation has come out slightly lower‑than‑expected at 3.3% in the US pushed some market participants to expect the interest rate cut on the other side of the Atlantic, too, this year. FED appears to agree with this outlook, although the extent of interest rate cuts in the US might still be much smaller than the markets were expecting in the beginning of the year.

Market view

As could have been expected, this year the outcomes of the many elections held in multiple jurisdictions mean volatility is back in the financial markets, as investors take the chances to adjust their positioning on the changing political landscape. While the central banks’ policy trend appears to be taking the long‑waited shape, the markets may yet be frustrated with the unwillingness of monetary policy makers to cut the rates more aggressively, as economic - and political – trends do not necessarily favor that.