Equity markets set convincing new highs | Luminor

Equity markets set convincing new highs

- Major equity markets on the rise

- The U.S. economy is still strong

- Bank of Japan ends negative rates era

In March, equity markets have surged to new highs, with the S&P 500 showing its strongest start since 2019, supported by notable performance from tech giants. Additionally, other developed market equities have continued to do well this year as the likelihood of recession recedes. However, alongside this optimism, caution is warranted in the short term due to potential market volatility and some signs of economic slowdown. Meanwhile, central banks, including the Federal Reserve (FED), European Central Bank (ECB), and Bank of Japan (BoJ), have made policy decisions that are shaping the global economic outlook. Their actions have been a major focus in global markets for the past few years, and it seems they will remain so for some time.

As a result, developed markets’ stock index MSCI World has risen by 2.72%, while emerging markets stocks’ index MSCI Emerging Markets has surged by 2.43%. During the same period yields on bonds have decreased slightly, with 10‑year US Treasury bond yields declining to 4.2% (compared to 4.25% 1 month ago) and German 10‑year bond yields decreasing to 2.29%, down from 2,41% a month ago.

Equity markets set new highs

The S&P 500 has had its strongest start since 2019, surging by approximately 10% and marking another record high for the year. The mega‑cap tech stocks such as Microsoft, Apple, Alphabet, Meta Platforms, Amazon and Nvidia have kept the lead in the rising market by gaining around 17% year‑to‑date, driven by excitement around artificial intelligence (AI) and robust earnings’ trends. Traditionally, a strong early performance often signals well for the market's prospects throughout the remainder of the year. However, this promising beginning is sparking some caution for the short term. This caution stems from the fact that much of the positive news may already be reflected in the current market prices, making it sensitive to any unexpected downturns in earnings or the economy.. Additionally, one must be reminded that the equity market typically experiences three to four drops of 5% or more each year, and the last significant pullback in the S&P 500 index occurred in October 2023, only, as many investors have been evidently confident in the future prospects.

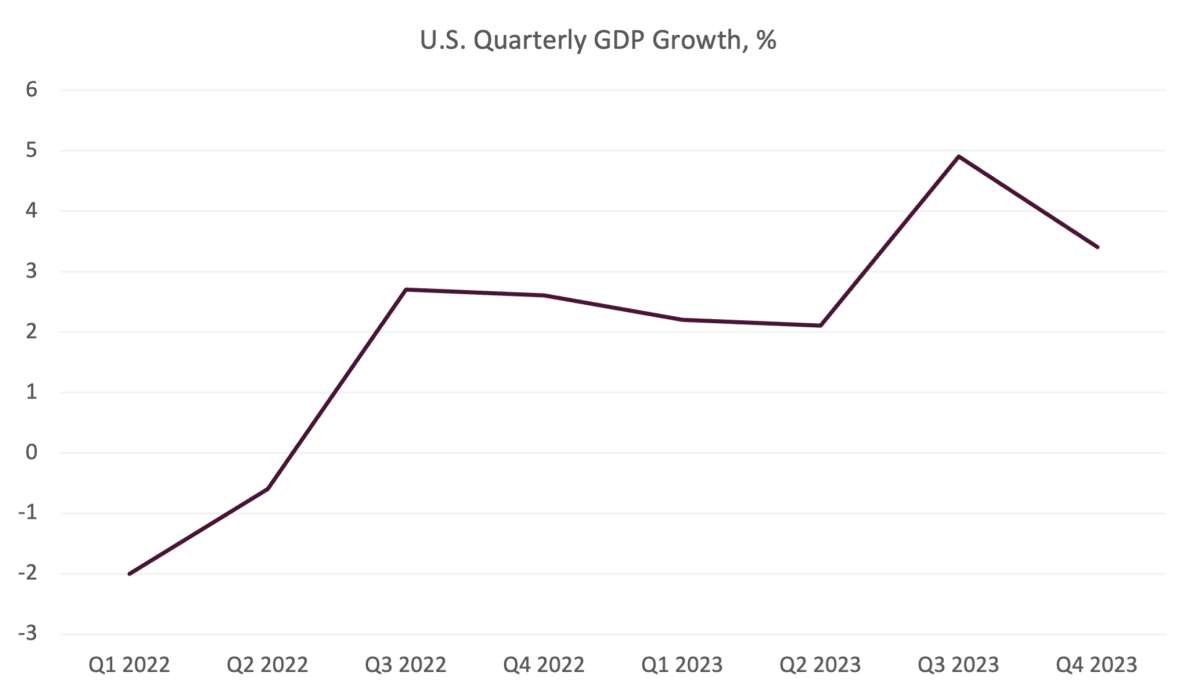

The U.S. economy is still doing well

The U.S. economy has seen two consecutive quarters of robust GDP growth exceeding 3%, (see Chart) leading to diminishing recession concerns. This stability is supported by strong consumer fundamentals, including record‑high household net worth and a growth in personal incomes. However, there are signs indicating a potential slowdown in growth. For instance, there has been a significant increase in credit card debt, record‑high borrowing rates, and a rise in credit card delinquencies. Additionally, both consumer and business confidence have slightly decreased since the beginning of the year. Despite these warnings, the labor market remains resilient, with strong job growth in the first months of the year. The inflation has decreased throughout 2023, but there has been a recent uptick in the past few months, which may prompt policymakers to remain cautious in their interest rate cut considerations. However, a sustained reacceleration in inflation seems unlikely due to decreasing global commodity prices, normalized supply chains, and consumer resistance to price hikes. Overall, while inflation may experience some fluctuations, it is unlikely to significantly alter the Fed's inflation forecasts to reach 2%.

Updates from Central banks

As expected, the FED closed out its March meeting by holding the federal funds rate at its current target range of 5.25%‑5.50%. This decision marks the fifth consecutive FED meeting where the central bank decided to keep interest rates at their current levels. As indicated in the updated Summary of Economic Projections (SEP) and “dot plot,” rate cuts remain on the horizon, with the Fed forecasting three 0,25% cuts occurring by this year’s end. No specifics were given as to when cuts would begin, with Chair Powell reiterating that all monetary policy decisions are made “meeting by meeting.” Markets reacted favorably to the Fed’s rate cut projections, with the S&P 500 moving above 5,200 for the first time.

The European Central Bank (ECB) and the Bank of Japan (BoJ) also held policy meetings last month. The ECB held rates unchanged, but its chief Christine Lagarde said discussions over easing policy have begun and plenty of relevant information would become available by June. Meanwhile, the BoJ made a notable move by raising interest rates for the first time in 17 years, from ‑0.1% to 0.1%, ending the world's only negative interest‑rate regime. BoJ policymakers reiterated in a post‑meeting press conference that a gradual approach will be taken to any further rate hikes, signaling that financial conditions will likely remain accommodative in the near term. Despite this significant decision, the overall market reaction was fairly muted, as markets had largely anticipated a rate hike.

Market view

Overall, central banks are expected to continue playing a key role in shaping financial markets in the near future, especially with decreasing inflation and the potential for interest rate cuts later this year. While the economy appears to be heading towards a soft landing, it is premature to declare mission accomplished. With a lot of good news priced in the current financial markets valuations, the investment team remains cautious of the potential volatility ahead.