Central banks have played Grinch this Christmas | Luminor

Central banks have played Grinch this Christmas

- Major indexes turn lower in December

- Japanese central bank surprises the markets, others stay hawkish

- Inflation subdued even further, while macro challenges remain

The year‑end rally has not materialized in the major stock markets around the globe, as investors have been assessing the policy updates from the leading global central banks. Global gauge of the developed markets companies’ stock prices – MSCI World Index – turned negative, falling 4,2% in December. In the meantime, MSCI Emerging Markets index, which captures the stock price changes of the companies in the developing markets, dropped by 1.6% .

FED slowing down

As we’ve been noticing throughout the remarkable year of 2022, the primary focus during December has stayed on the inflation and the central bank limbo. The Federal Reserve (US Central bank) has raised the interest rates once again during its meeting in December. The slight change of tone in numeric decision (0,50% increase) has somewhat contrasted with the comments by the central bank’s statement and the policymakers’ projections on the peak interest rate level for the next year.

ECB on track to further hikes

On the other side of the Atlantic, ECB raised the interest rates (as expected in our December newsletter) by 0.50 %. Financial markets took a lower turn after the Head of ECB, Christine Lagarde, shared her anticipation of another 50 basis‑point rise at the next meeting on Feb 2 "and possibly at the one after that, and possibly thereafter". Naturally, some investors have been caught off‑guard by the strictness in tone and that has spelled the correction in the European assets and once again rising yields.

Japan central bank surprising the markets

However, arguably the largest surprise came from Japanese Central Bank (JCB), which caught investors completely off‑guard by announcing its decision to widen the accepted channel for the yields on the 10‑year bonds when implementing its monetary policy. Contrary to the assurances from the JCB itself, market participants have read the decision as a sign of pivot away from multi‑year long ultra‑dovish monetary policy. As a result, Japanese yen jumped by 4% versus US Dollar for the day, while Japan’s Topix equity index dropped by 1,5%, as investors regarded that as yet another chapter in the global tightening cycle.

Inflation subdued, macro challenges remain

On a positive side, the inflation figures have been trending down across the developed markets. While that may herald some inspiration to the financial market participants, it is obvious that the elevated inflation rates are going to haunt the global economy for the foreseeable future. With some macroeconomic news still rolling in a rather resilient mode (see the “Change in Nonfarm payrolls” data in the US, below), it is likely that some investors will be reading positive macro news as market‑negative, as it may draw additional action by the central banks in 2023.

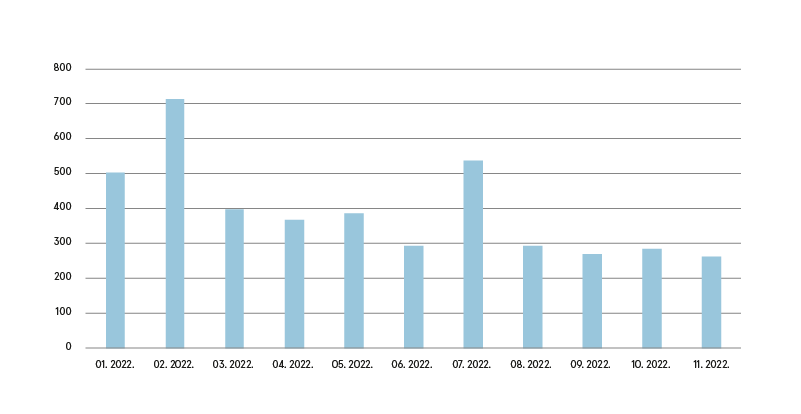

Change in Nonfarm Payrolls in the US

Source: Bloomberg L.P.

“House view” update

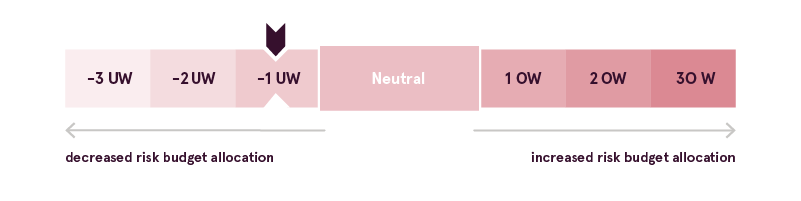

The neutral risk allocation budget, which was re‑stated in November, was left intact in December. With the tightening cycle and the 2022‑prevalent trends still in strong mode, we remain constructive on the defensive sectors, holding the tactical exposure to utilities, energy, and consumer staples.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.