Markets corrected after reaching record highs | Luminor

Markets corrected after reaching record highs

- New COVID variant spooked investors

- Central bank taper decisions in focus

In the first half of November equity markets continued to reach new highs, but during last weeks of the month, momentum faded and indexes consolidated for a while. In the end of the month, volatility spiked and equity indexes experienced a sharp decline after the new COVID-19 variant was identified in South Africa, which could be more transmissible than other variants. Together with surging COVID cases in Europe, it raised fears of another wave of lockdowns. For example, Austria had already reimposed a full lockdown, prior to the new variant, while Germany warned it may follow suit.

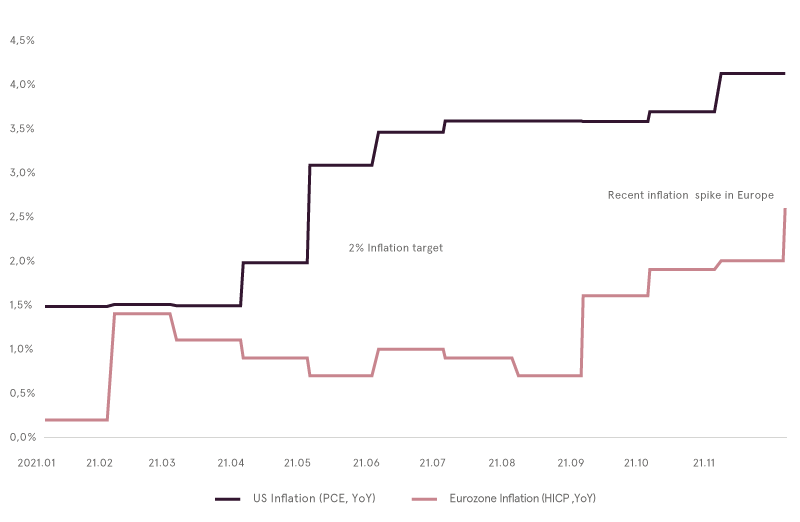

Newest data shows mounting pressure for central banks to act, as rising prices pushed higher above 2% inflation target. US Federal Reserve (FED) president Jerome Powell told, that it is time to retire word “transitory”, when talking about inflation and opened doors for sooner than expected rate hikes. Preferred inflation ratio by the FED is Personal Consumption Expenditures (PCE), which measures goods and services targeted towards and consumed by individuals and uses slightly different calculation methodology, than the widely known Consumer Price Index (CPI). Meanwhile, in the euro area, the Harmonized Index of Consumer Prices (HICP) is used to measure inflation.

Inflation in US and eurozone

Source: Bloomberg Finance L.P.

Markets cautiously evaluated the US President’s decision to reappoint Jerome Powell as a chairman of the Federal Reserve for a four year term beginning next February. Investors and analysts expect continuation of the current policy – anticipating FED rate hikes starting mid-2022 and preparing for diminishing support for the US economy as FED started to pare its monthly asset purchases by 15 billion USD each month.

In the Financial Stability Review, ECB warned, that stretched prices in property and financial markets, as well as high debt levels in corporate and public sectors pose a threat to the euro-area stability. ECB pointed out, that the pandemic continues to be one of the main risks to economic growth, as disruptions to global supply chains and possibility of new lockdowns to stem the latest virus wave present fresh challenges. The Central bank also mentioned about the risks posed by stubbornly high inflation, but did not elaborate on monetary policy before the key meeting in December. Persistent high inflation levels could translate into an untimely tightening of financial conditions, weighing on the economic recovery.

One positive development was observed in November, when the US President Joe Biden and the Chinese President Xi Jinping had a virtual summit, with both sides aiming to stabilize the relationship between the two nations. No major breakthroughs have been achieved, but it still indicates, that both sides are willing to avoid conflicts between the world’s two biggest economies, as tensions built up over a wide range of issues, including tariffs, sanctions and human rights. Xi came to the summit with a strong position, having recently secured his third term as a Communist Party Chief. Meanwhile, Biden signed infrastructure bill into law, which should boost US competitiveness with China.

It seems, that prior to the crucial year-end period, stores were able to ship goods despite supply chain bottlenecks, while shipping rates started to ease across the world. Rates paid for the transport of dry bulk materials necessary to produce goods reached a peak in October and declined more than 50% since then, while a price to ship containers from China to US and Europe declined 10-16% over the same period. Hopefully, this trend will persist in 2022, helping to contain inflation.

Shipping costs started to go down

Source: Bloomberg Finance L.P.

More encouraging news about the state of the consumer comes from the new records reached during the Singles Day (11.11) event, which was pioneered by Alibaba in 2009 and has become one of the biggest shopping events globally. Alibaba gross merchandise volume (GMV) grew 8% (YoY) to ~ 84.5 billion USD during the 11-day period, while JD.com’s transaction volume during Singles Day period increased by 28% (YoY) to almost 55 billion USD. In US, retailers witnessed shift in consumer behavior as sales were more distributed throughout November and not concentrated during Black Friday and Cyber Monday events.

“House view” update

Our investment team still thinks that a lot of positive and negative factors currently warrant neutral risk allocation. The new COVID-19 variant and a higher probability of full lockdowns, a rise in volatility and diminishing support from central banks provide reasons to be cautious. On the other hand, present fiscal and monetary stimulus, favorable end-of-the-year period and encouraging retail sales provide ground to be cautiously optimistic.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.