Markets bounced back to all-time highs | Luminor

Markets bounced back to all-time highs

- Markets recovered from a minor correction

- Inflation expectations reached new highs

- High probability of a year-end rally

Mild correction, which took place in September, was widely expected, as 5% corrections in the S&P 500 index typically occur three to four times a year, larger corrections of more than 15% happens on average once per two years. Yet, investors have not seen a 10-20% correction in the S&P 500 index already for more than 400 days.

Looking on the bright side, the 4th quarter is typically known in the markets as a year-end or “Santa Claus” rally period, as profits are boosted by increased spending in order to prepare for Christmas and New Year. According to the US National Retail Federation’s (NRF) forecast, sales growth in November-December this year are expected to hit record levels, reaching 8.5-10.5%, as major consumer goods makers and retailers work hard to prevent supply chain disruptions and avoid empty shelves during the gift season. Thanks to the rising incomes and stronger than ever household savings, consumers are expected to spend more on goods, while rising inflation will contribute to higher spending value.

After the brief pullback in September, markets rebounded sharply and many equity indexes reached new record highs. Investors’ willingness to “buy the dip” was lifted by strong corporate earnings during the third quarter. Moreover, concerns about the Chinese real estate market meltdown subsided after the local central bank assured, that it can contain risks, which are rising from the troubled real estate developer Evergrande. Local authorities also pressured the founder of Evergrande, billionaire Hui Ka Yan, to use his personal wealth to pay off the company’s debt. This fact demonstrates the unwillingness of the Chinese government to rescue the company and its continuous crackdown on the upper class. It is unclear, whether Hui Ka Yan’s assets could make a dent in the Evergrande’s 300 billion USD debt.

During October, many companies started to announce their third quarter results, which in many cases were better than anticipated. At the time of making this overview, 363 out of 500 S&P 500 index companies reported their results, according to Bloomberg LP data. On average, these companies announced that third quarter sales grew almost 18.5% (Q/Q), while earnings increased roughly 39.4% (Q/Q). In Europe, earnings were also strong – 272 out of 442 Euro Stoxx 600 index companies reported 14% (Q/Q) sales growth and 51.4% (Q/Q) earnings growth.

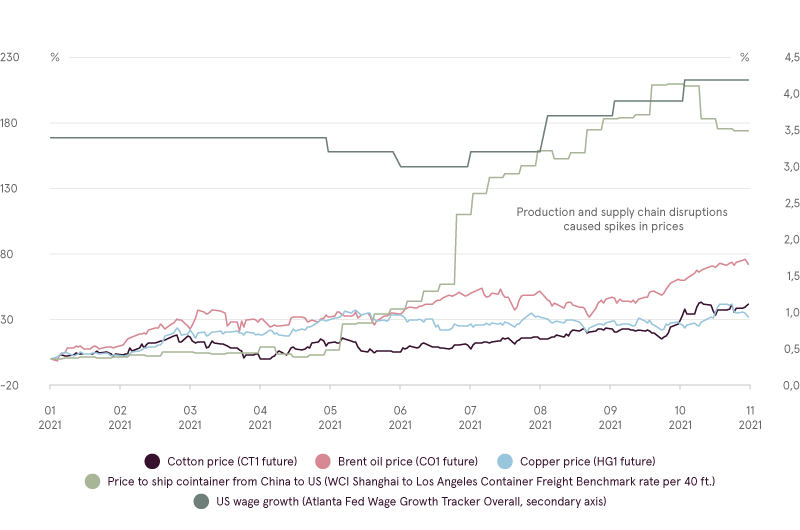

Commodities, wage growth and supply chain bottlenecks

Source: Bloomberg LP

Rallies in oil prices and other commodities added to inflationary pressures, while wage growth in the US was reaching highest levels in more than a decade. Regardless of recurring statements by central banks, that the rise of products and services prices is transitionary and will ease in 2022, central banks could be forced to start raising interest rates sooner than expected, if inflation continues to overshoot.

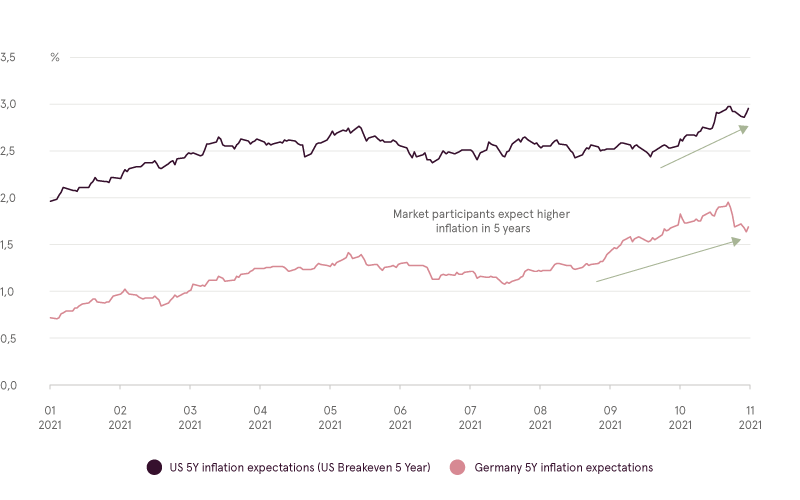

It seems, that market participants started to lose faith in the transitory inflation narrative. This can be clearly seen in the US 5-year inflation expectations1, which reached 16-year highs last month. Higher than expected inflation opinion is supported by producers of consumer staples like Unilever. The company’s finance chief told that they expect inflation to be higher next year than in 2021. Unilever makes fast-moving consumer goods, such as soaps, detergents, food products, etc. One of the biggest food makers Nestle announced that they plan to increase product prices as prices of raw materials keep on climbing. It is not yet clear, which scenario is more probable. In the case of a swift recovery of the global supply chains, shortages would disappear and inflation would diminish to normal levels. For instance, freight rates from Shanghai to Los Angeles seem to have reached an interim peak and corrected slightly. On the other hand, if high inflation rates persist and central banks start to tighten monetary policy, higher interest rates could trigger re-evaluation of risky assets.

5Y inflation expectations

Source: Bloomberg LP

“House view” update

During the correction and rebound phase, we remained at Neutral risk allocation. Most indicators and models, which deteriorated during the pullback in the markets, rebounded nicely, but still, they did not warrant going overweight just yet. There is a high probability, that optimism will continue to push indexes higher until the end of the year, as we enter seasonally good period. We are continuously assessing the situation in the markets and will make adjustments if needed.

15 year inflation expectation rate is calculated by subtracting the real yield of the inflation linked maturity curve from the yield of the closest nominal Treasury maturity.