Market sentiment swings wildly | Luminor

Market sentiment swings wildly

- Market pullbacks often seem more severe than they truly are

- The swings in Japan

- Markets focus on Federal Reserve symposium in Jackson Hole

Although minor cracks in the economy have been emerging, growth has remained resilient until now. This resilience is why the market, until recently, largely anticipated a soft landing. However, last month’s unexpectedly weak US jobs report, sluggish manufacturing activity, and a rise in the unemployment rate to 4.3% have altered that narrative. With a soft landing now uncertain, equities tumbled, bond yields dropped to their lowest level since 2023, and the market quickly priced in over 100 basis points of rate cuts by year‑end. Conversely, financial markets have rallied since the August 5 sell‑off, with major indexes rebounding strongly. Market narratives can shift rapidly, but they are not always accurate – this has occurred multiple times during this cycle, and it could happen again.

As a result, developed markets’ equities (measured by MSCI World index) have risen 0.34%, while emerging markets’ equities (measured by MSCI Emerging Market index) declined 0.66%. During the same period, yields on bonds have decreased, with 10‑year U.S. Treasury bond yields declining from 4.03% a month ago to 3.9%, while German 10‑year Treasury bond yields remained steady at 2.3%.

Pullback in markets

Market declines, regardless of size, can feel unsettling. The 3% drop in the S&P 500 at the beginning of the month drew significant attention and caused anxiety. In contrast, the 3% rally in early July and the more than 2% rise in the final days of that month likely didn’t resonate as strongly, highlighting how pullbacks tend to have a greater psychological impact. It’s crucial to remember that the recent pullback came after the market had reached record highs, with recent lows leaving the S&P 500 just 8% below its all‑time peak. The frenzy of market volatility can easily cause investors to lose sight of the bigger picture. During a pullback, it may seem like a major event or something unusual is happening, but historically, declines of 5% or more typically occur about three times a year. However, taking a step back shows that despite the recent dip, the stock market remains up nearly 20% from last year and 50% since the start of this bull market in October 2022.

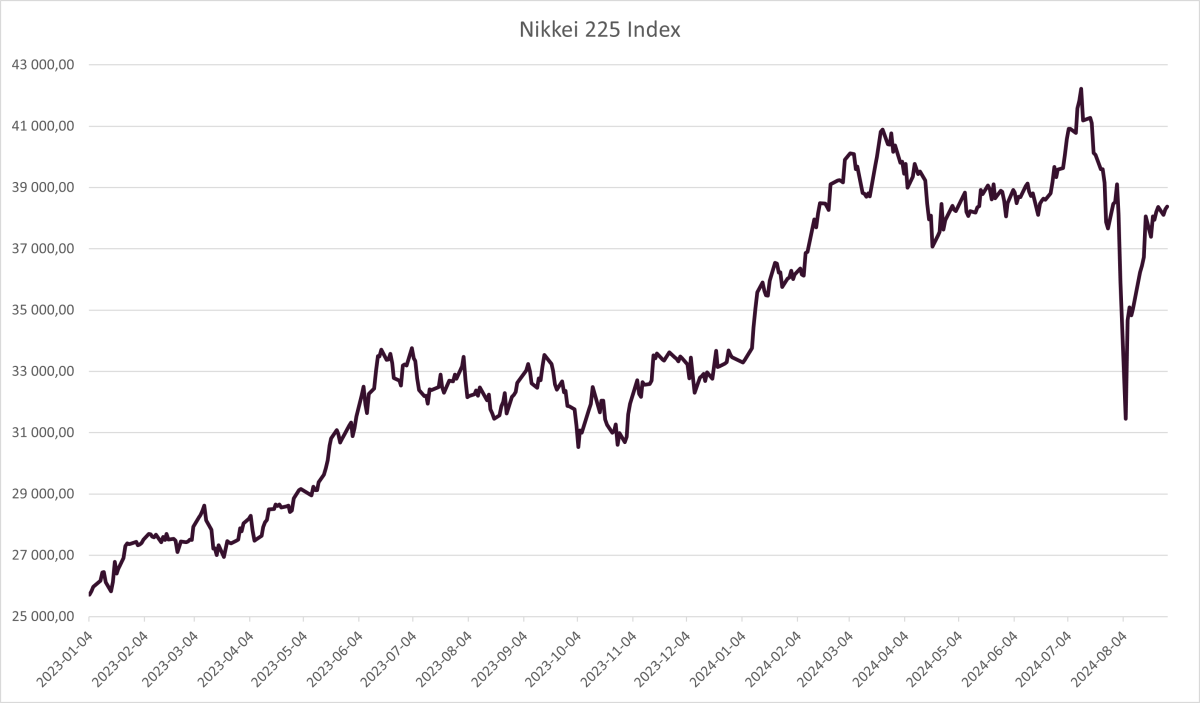

Nikkei 225 suffers historic drop

At the beginning of the month, the Nikkei 225 index, a benchmark for leading stocks in Japan, experienced one of its biggest drops in history. In percentage terms, the index closed down more than 12%, marking its largest one‑day fall since October 1987. Analysts suggested that one potential reason for this sharp decline could be the unwinding of yen‑funded carry trades. This practice involves borrowing money in a country with low interest rates, like Japan, and investing it in assets elsewhere that offer higher returns. Additionally, the U.S. market often influences other global markets, and part of the decline in the Japanese market may have been due to catching up with losses in the U.S. market. Meanwhile, Japanese investors were revising their bets in the wake of unexpected Bank of Japan’s decision to raise the interest rates to “around 0,25%” from the previous range of “0% to 0,1%”, triggering panic. According to Reuters, most analysts believe that neither interest rate expectations nor economic data fully explain the severity of the sell‑off. Instead, it was likely driven by the rise in the yen, which, with its near‑zero short‑term yields and steady depreciation, had long served as a funding currency for billions of dollars worth of investments.

Source: Investing.com

Federal Reserve (Fed) signals readiness for rate cut

Policymakers have been considering the right time to begin easing their restrictive policy stance for nearly a year. However, with growth moderating, the labor market cooling, and inflation risks diminishing, the conditions now seem favorable for a rate cut of at least 25 basis points in September. As market participants had anticipated, Jerome Powell used his platform at the Jackson Hole Symposium to deliver the signal that the time has come for the Fed to start moving the fed funds rate lower. While he did not specify the size or pace of the cuts, Powell highlighted a moderation in inflation and a softening labor market. He expressed increased confidence that inflation is on track to reach 2%. It is now expected that the Fed will cut the federal funds rate by 0.25% in September, reducing it from the current range of 5.25% to 5.5%, and implement two to three rate cuts throughout 2024, in total. Although the market anticipates an aggressive and rapid easing cycle over the next year – the actual pace and extent of the Fed’s rate adjustments will depend on the forthcoming economic data.

Market view

The recent stock market recovery has once again been driven by the technology and growth sectors, which were the hardest hit during the recent pullback. As we approach a period of potential Fed rate cuts, with inflation moderating and earnings growth extending beyond just technology and growth sectors, a broadening of market leadership could be anticipated. Although market fluctuations are common, especially as we head into the seasonally weaker months of September and October, and then into the U.S. elections, these periods of volatility and pullbacks may be seen by market participants as potential opportunities.