Donald Trump’s action movie | Luminor

Donald Trump’s action movie

- Trump’s tariff chaos – Mexico, Canada, China and others in the spotlight

- Federal Reserve (FED) to slow down on interest rate cuts this year

- China’s equity market alive and investable again?

February has brought some wild swings to the financial markets. This was mostly backed by the busy – sometimes chaotic – political agenda for the month as well as lingering somewhat subdue sentiment among the investors. The markets have been struggling to find a direction as some of the major macroeconomic policies of major markets – mostly US – were put into question, with investors left to guess the economic impact of some highly uncertain policymaking decisions.

As a result, developed markets’ equities (measured by MSCI World index in EUR) have dropped by 0.86%, while emerging markets’ equities (measured by MSCI Emerging Market index in EUR) have gained 0.44%. During the same period yields on bonds were declining, with 10‑year U.S. Treasury bond yields decreasing to 4.23% from 4.53% a month ago, while German 10‑year Treasury bond yields have declined to 2.39% from 2.46% a month ago.

Trump’s busy agenda

Having been sworn in as a returning president only in late January, President Trump has been implementing his action plan during the month of February at full speed. Among the many initiatives that the new US presidential administration is keen on implementing, investors, so far, have paid most of the attention to the tariff agenda. The implementation of that agenda has proved to be nothing short of an action movie in February. Fresh from his tariff spat with the neighboring Colombia over immigration topics, Trump has hit out at some of the most important trading partners of the US – Mexico, Canada and China – by threatening to impose the unilateral tariffs on these countries before retracting some of the planned action after late‑minute calls with the respective leaders. In addition to that, at the end of February, President Trump has aired the idea of imposing 25% tariffs on the EU imports, too. Coupled with the open‑ended tariff saga on the Mexico, Canada and China trio, this potential disruption of the international trade is weighing heavily on the market expectations of the investors and will continue this way for the coming months.

FED on the spotlight

Financial market participants have long been cautious about the insistence of Donald Trump to offer pointed suggestions to the FED on policy making. As the political interference in the monetary policy is usually better associated with some selected Emerging Markets, the decaying governance of the largest economy in the world would pose serious risks to the market itself as well as the primary reserve currency, which is the US Dollar.

These fears have been put somewhat to rest for now, as the Treasury secretary has clarified some of the previously expressed views by the newly‑elected president Trump that the interest rate that the administration is mostly focused on is the 10‑year Treasury bond yield, rather than the short‑term key policy rate set by the FED.

In the meantime, lingering uncertainty of the potential tariffs and their impact on the US inflation is starting to lift the inflation expectations. As a result, market participants have been changing their expectations for the interest rate cuts by the FED this year. From what was the largely the consensus view by the many analysts of two 0,25% interest rate cuts by the FED, some analysts have been trimming their expectations down to single 0,25% interest cut in 2025, only.

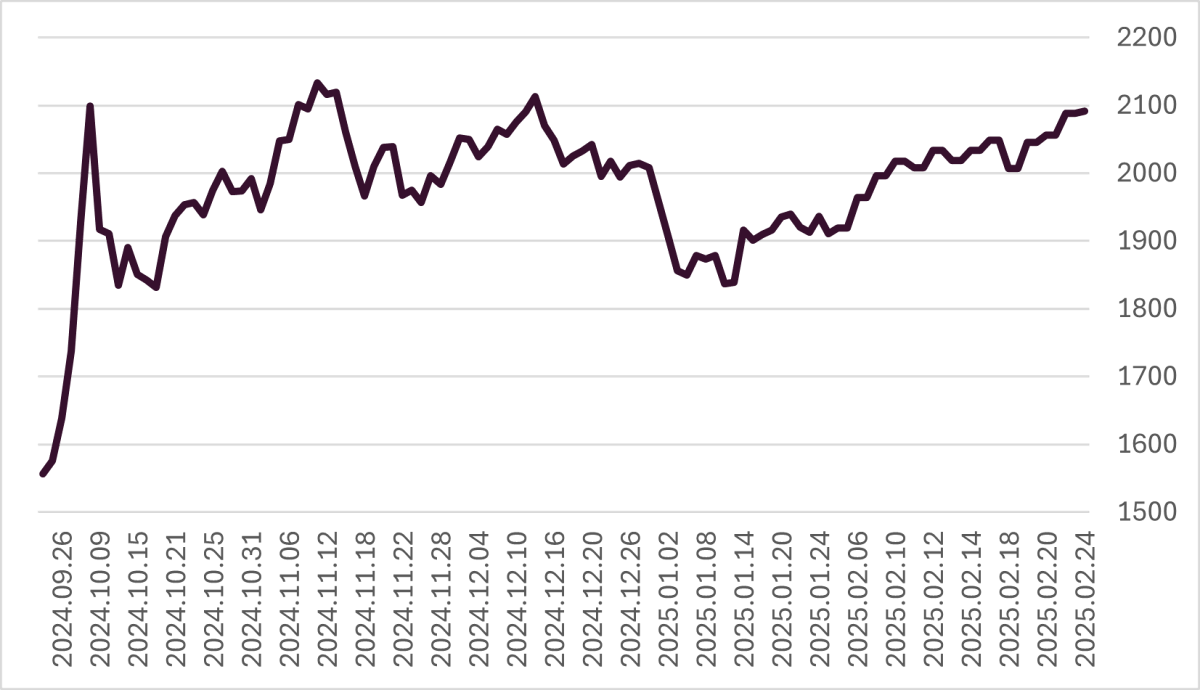

Chinese equity SZSE index

Source: investing.com

China’s bounce back

In recent years Chinese equities have been under sustained pressure, thanks to multiple macroeconomic issues the local stock market is facing and the apparent political interference in some of the key developments in the Chinese technology industry.

While the incremental stimulus has reignited some of the excitement back in the Chinese equities’ market in 2024 October, the sentiment has been somewhat stabilized on the back of the uncertainty of Donald Trump administration agenda as well as the worries surrounding its seemingly lagging AI capabilities.

Since the public launch of AI tool Deepseek in late January, some investors apparently got much less concerned about the AI capabilities of the Chinese technology sector, piling into local equities once again. February brought some very welcome news, too, to those concerned about the political interference as one of the most prominent businessmen and national tech champion – Alibaba – founder Jack Ma has appeared at the government symposium, having been out of public sight since 2020 after criticizing government regulations.

As a result, investors took the local equities to higher levels, almost exceeding the highs of October (see chart).

Market view

So far, Donald Trump is proving to be a truly disruptive factor in assessing the financial markets’ prospects, as the policy announcements appear to follow random walk with add‑on changes, postponements or even cancellations. While market participants will have a lot of troubles guessing and re‑assessing the Trump’s next moves, financial markets should experience increased volatility.

As the Chinese equities are recovering from the knockdown of recent years and months, macroeconomic headwinds and policy uncertainties will keep the valuations at a discount compared to the developed stock markets. The size of that discount is bound to get reassessed by the investors, should China be able to address some of the key concerns going forward.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.