2021 – year of COVID waves, record high stock market indexes and not exactly “transitory” inflation | Luminor

2021 – year of COVID waves, record high stock market indexes and not exactly “transitory” inflation

- Rising inflation influenced changes in central bank monetary policy

- Omicron wave threatens the world

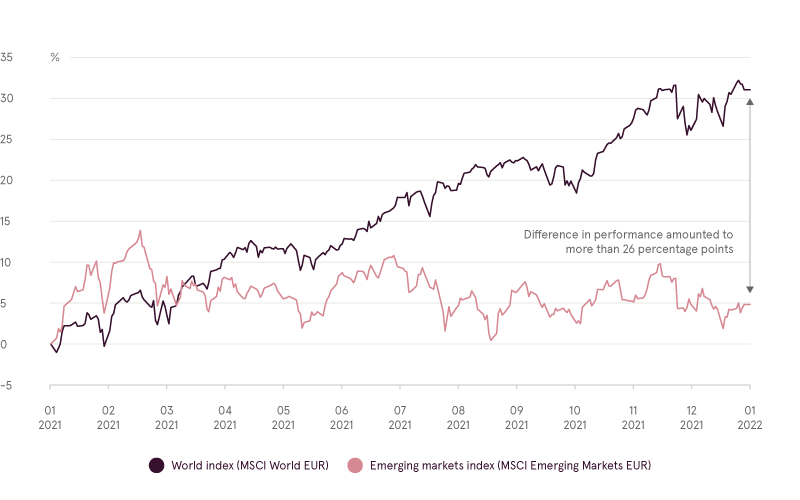

In December 2021, the MSCI World index in euros rebounded 3,2% and ended the year with a 31% increase, while the emerging market index in euros increased in 2021 only by 4,9%. Such return dispersion was evident not only when comparing regions, but also inside the US, which showed one of the best performances this year. To illustrate, the S&P 500 index in euros rose by 36%, while small caps (Russell 2000 index in euros) posted only a 22% increase. Furthermore, the pandemic darling ARKK ETF, which invested in some of the most popular “lockdown” growth names like Zoom Video Communications, Teladoc Health, Peloton Interactive, Tesla and others, recorded a 24% decline over the year, after reaching a peak in February 2021.

Equity markets in 2021

Source: Bloomberg LP

Investors waited for December central bank meetings with concern expecting announcements to cut bond buying programs and indications of potential rate hikes sooner than expected. The Bank of England was the first from G7 countries to raise interest rates from 0,1% to 0,25%. The US Federal Reserve (FED) chairman Jerome Powell signaled, that high inflation has become a major concern, which could derail the country’s economic expansion. Such statement contrasts to previous rhetoric, that inflation is transitory due to supply chain bottlenecks, which soon would fade away. Furthermore, FED sped up the tapering of its asset‑buying program, while projecting interest rate hikes in 2022.

Meanwhile, the European Central Bank (ECB) temporarily extended its regular monthly bond purchases to smooth the phasing out of the pandemic stimulus. Thus, the Asset Purchase Programme will be doubled to 40 billion EUR a month in the second quarter of 2022, before gradually returning it to 20 billion EUR in October 2022. This should help to cushion a 1,85 trillion‑euro emergency program exit in March 2022. The ECB expects a strong economic rebound coupled with higher levels of inflation. According to the ECB projections, the inflation rate is expected to decrease to 3,2% in 2022, before falling below the 2% target in 2023.

On 15 December 2021, China reduced the reserve requirement by 0,5 percentage points to 8,4% for most banks, hence, releasing 1,2 trillion yuan (~188 billion USD) of liquidity. It was the second reduction this year, with the central bank aiming to mitigate the worsening situation in the real estate market. One of the biggest real estate developers in the country Evergrande was officially labeled a defaulter and local creditors have sued company for more than 13 billion USD in allegedly overdue payments. There is a major concern, that Evergrande’s default could cause a real estate meltdown in the country or even affect stability of the global financial system, because the company’s debt exceeds 300 billion USD. Moreover, there have already been signs of the spreading contagion in the Chinese real estate market, with smaller real estate developers having liquidity problems and announcing defaults.

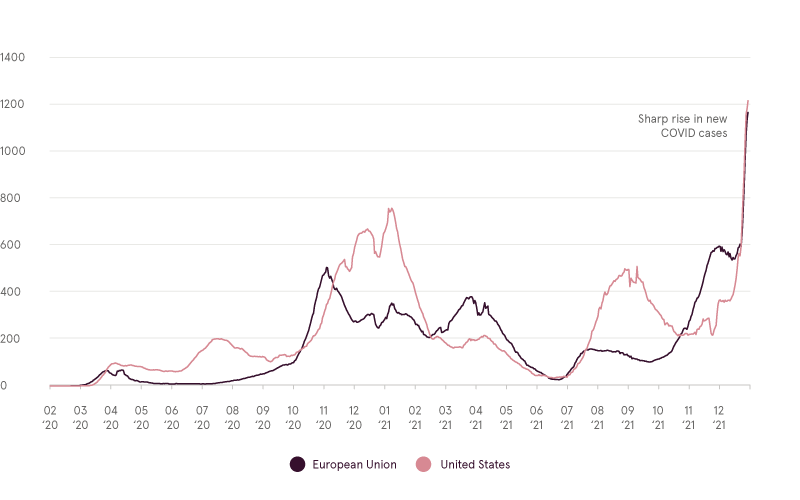

New COVID cases per million people

Source: Johns Hopkins University CSSE COVID‑19 Data

The rapidly rising new COVID‑19 cases could still affect manufacturing and produce even more bottlenecks. The potential introduction of new lockdowns, in order to prevent occupancy rates in hospitals from rising, pose the largest threat to the economic recovery. Nonetheless, although the quickly spreading Omicron variant threatens to cause more challenges, booster shots and rising vaccination rates help to remedy the situation. Moreover, the latest data shows, that the average case fatality rate in the EU and the US dropped by half since the end of October 2021.

“House view” update

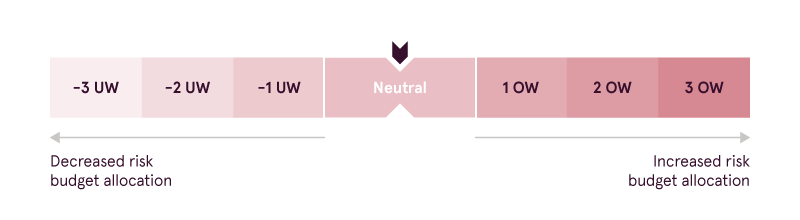

The Luminor investment team maintained neutral risk allocation. The year‑end rally raised the world equity index to new highs, yet changes in monetary policy and rising new COVID‑19 cases provide enough reasoning to remain cautiously optimistic.

Warnings:

- This Marketing Communication is not considered investment research and has not been prepared in accordance with standards applicable to independent investment research.

- This Marketing Communication does not limit or prohibit the bank or any of its employees from dealing prior to its dissemination.

Origin of the Marketing Communication

This Marketing Communication originates from Portfolio Management unit (hereinafter referred to as PMU) – a division of Luminor Bank AS (reg. No 11315936, with registered address at Liivalaia 45, 10145, Tallinn, Republic of Estonia, hereinafter - Luminor). PMU is involved in the provision of discretionary portfolio management services to Luminor clients.

Supervisory authority

As a credit institution Luminor is subject to supervision by the Estonian financial supervision and resolution authority (Finantsinspektsioon). Additionally, Luminor is subject to supervision by the European Central Bank (ECB), which undertakes such supervision within the Single Supervisory Mechanism (SSM), which consists of the ECB and the national responsible authorities (Council Regulation (EU) No 1024/2013 - SSM Regulation). Unless set out herein explicitly otherwise, references to legal norms refer to norms enacted by the Republic of Estonia.

Content and source of the publication

This Marketing Communication has been prepared by PMU for information purposes. Luminor will not consider recipients of this Communication as its clients and accepts no liability for use by them of the contents, which may not be suitable for their personal use.

Opinions of PMU may deviate from recommendations or opinions presented by the Luminor Markets unit. The reason may typically be the result of differing investment horizons, using specific methodologies, taking into consideration personal circumstances, applying a specific risk assessment, portfolio considerations or other factors. Opinions, price targets and calculations are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioural technical analyses of underlying market movements in combination with considerations of the market situation, interest rate forecasts, currency forecasts and investment horizon.

Luminor uses public sources that it believes to be reliable. However, Luminor has not performed independent verification. Luminor makes no guarantee, representation or warranty as to their accuracy or completeness. All investments entail a risk and may result in both profits and losses.

This Marketing Communication constitutes neither a solicitation of an offer nor a prospectus in the sense of applicable laws. An investment decision in respect of a financial instrument, a financial product or an investment (all hereinafter “product”) must be made on the basis of an approved, published prospectus or the complete documentation for such a product in question and not on the basis of this document. Neither this document nor any of its components shall form the basis for any kind of contract or commitment whatsoever. This document is not a substitute for the necessary advice on the purchase or sale of a financial instrument or a financial product.

No Advice

This Marketing Communication has been prepared by Luminor PMU as general information and shall not be construed as the sole basis for an investment decision. It is not intended as a personal recommendation of particular financial instruments or strategies. Luminor accepts no liability for the use of the Marketing Communication content by its recipients.

If this Marketing Communication contains recommendations, those recommendations shall not be considered as an objective or independent explanation of the matters discussed herein. This document does not constitute personal investment advice or take into account the individual financial circumstances or objectives of the persons who receive it. The securities or other financial instruments discussed herein may not be suitable for all investors. The investor bears all risk of loss in connection with an investment. Luminor recommends that investors independently evaluate each issuer, security or instrument discussed herein and consult any independent advisors if they believe it necessary.

The information contained in this document also does not constitute advice on the tax consequences of making any particular investment decision. The estimates of costs and charges related to specific investment products are not provided therein. Each investor shall make his/her own appraisal of the tax and other financial advantages and disadvantages of his/her investment.

Risk information

The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to many different factors. The value of and income from any investment may fluctuate from day to day as a result of changes in relevant economic markets (including changes in market liquidity). The information herein is not intended to predict actual results, which may differ substantially from those reflected. Past performance is not necessarily indicative of future results. When investing in individual financial instruments the investor may lose all or part of their investments.

Important disclosures of risks regarding investment products and investment services are available here.

Conflicts of interest

To avoid occurrence of potential conflicts of interest as well as to manage personal account dealing and / or insider trading, the employees of Luminor are subject to the internal rules on sound ethical conduct, management of inside information, and handling of unpublished research material and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. Luminor’s Remuneration Policy establishes no link between revenues from capital markets activity and remuneration of individual employees.

The availability of this Marketing Communication is not associated with the amount of executed transactions or volume thereof.

This material has been prepared following the Luminor Conflict of Interest Policy, which may be viewed here.

Distribution

This Marketing Communication may not be transmitted to, or distributed within, the United States of America or Canada or their respective territories or possessions, nor may it be distributed to any U.S. person or any person resident in Canada. The document may not be duplicated, reproduced and(or) distributed without Luminor’s prior written consent.